Deposits held with a Canadian Insurance Company offer many features NOT available with Bank GICs, including:

- Estate Planning Benefits: You have the right to name “beneficiaries” on all accounts. You can designate different amounts for different beneficiaries and designate HOW beneficiaries might receive proceeds (i.e. lump sum or over a fixed term). These deposit contracts are designed to help transfer wealth to heirs quickly, privately, and cost-effectively. They typically by-pass the probate process and provincial legislation like BC’s Wills Variation Act.

- Potential Creditor Protection: Deposits held with a life insurance company may receive an “exemption” from creditors and litigants under certain conditions. Royal Bank of Canada v. North American Life Assurance Co., [1996] 1 S.C.R. 325e

- Potential Tax Advantages for Non-Registered Accounts: Age 65 or older? Interest from your non-registered GIA may qualify for the annual pension income tax credit. Accrued interest from your GIA or DIA may also be an eligible source of pension income for purposes of income splitting. You can learn more about potential tax advantages here and here.

- Competitive Rates: See below.

- Longer Deposit Terms: 1-10 year terms are available (banks maximum is 5 years).

- Diversify Risk: Deposits are guaranteed up to $100,000 per account type (i.e. registered/non-registered) by ASSURIS – (the insurance equivalent of the CDIC). It extends guarantees to deposits held with a bank.

IA Financial Guaranteed Interest Accounts – November 25, 2022.

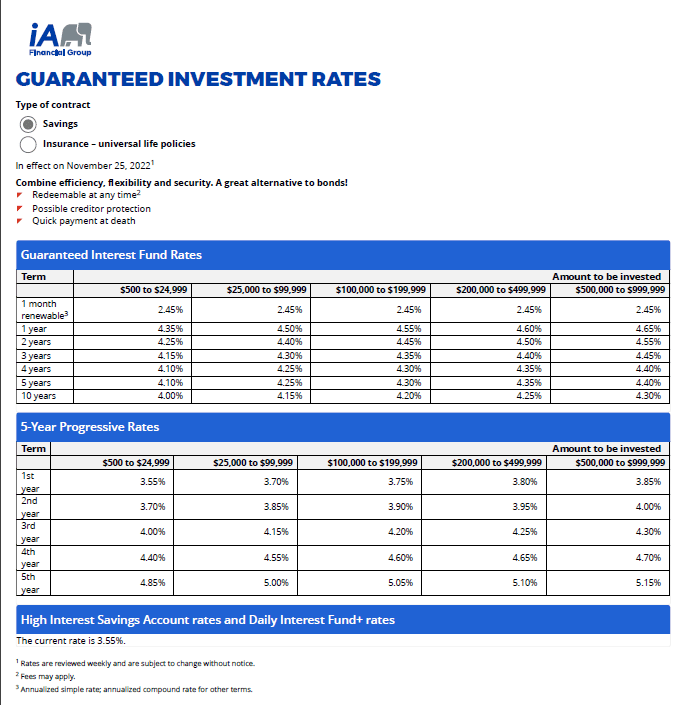

IA Financial – Guaranteed Investment Rates – Savings Nov 25, 2022.

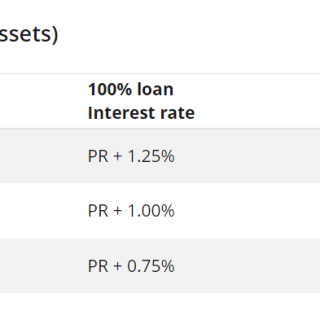

IA Financial Lending Rates – November 18, 2022.

Prime Rate November 25, 2022 – 5.95%

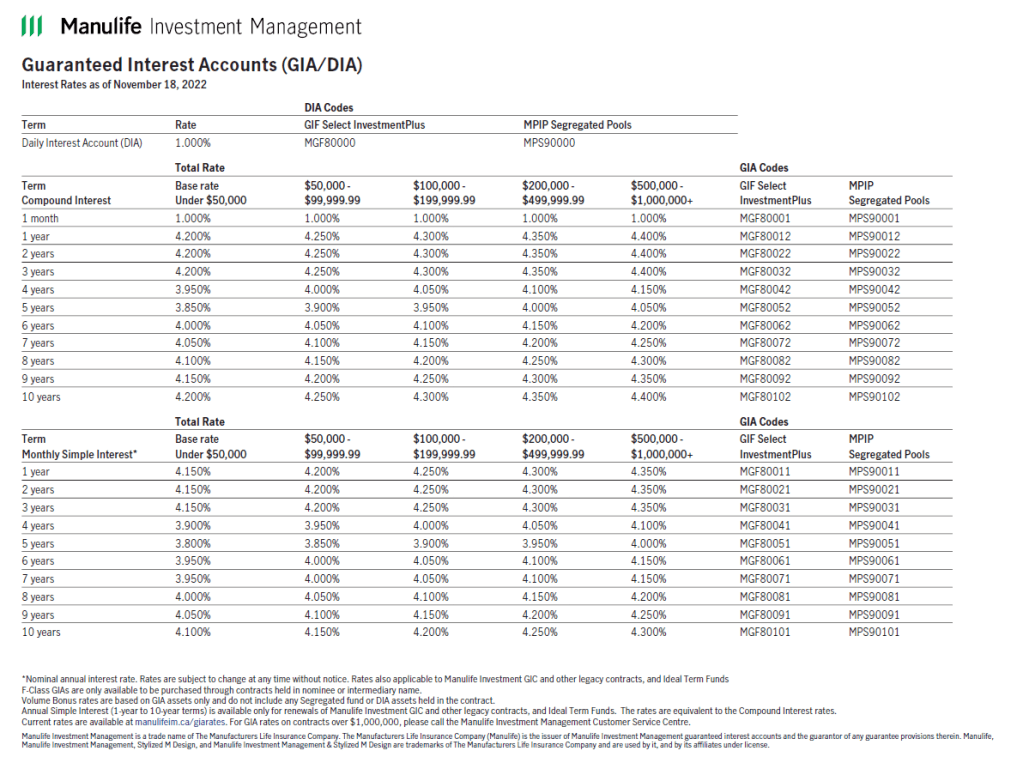

Manulife Guaranteed Interest Accounts – November 18, 2022.