If you understood a business perfectly and the future of the business, you would need very little in the way of a margin of safety. SO, the more vulnerable the business is, assuming you still want to invest in it, the larger margin of safety you’d need. IF you’re driving a truck across a bridge that says it holds 10,000 pounds and you’ve got a 9,800 pound vehicle, if the bridge is 6 inches about the crevice it covers, you may feel okay, but if it’s over the Grand Canyon, you may feel you want a little larger margin of safety.”

Warren Buffett, 1997 Berkshire AGM

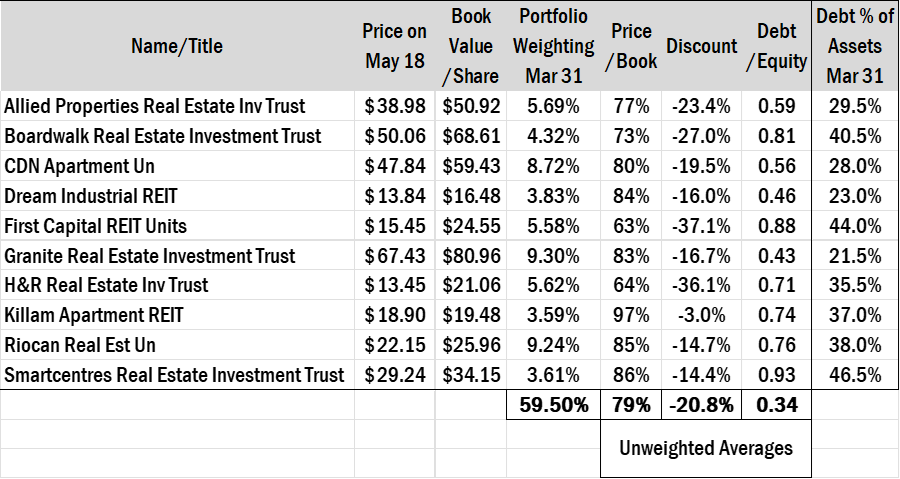

Over the past few days, I’ve been posting the first quarter operating results of top ten REITs from our property portfolio.

Most of the REITs have reported satisfactory results. They’ve all survived the pandemic and now they’re emerging as expected. Revenues, Net Income, FFO (Funds from Operations), SPNOI (Same Property Net Operating Income) and Occupancies were up for the most part. Outstanding rents have been recovered. Most are proceeding with further development of their pipelines.

A couple of exceptions bear note. Figures at H&R REIT were a bit abnormal. Last Summer, H&R REIT sold the Bow to affiliates of Oak Street Real Estate Capital. “The Bow” is one of the tallest buildings in Western Canada and it was a crown jewel in H&R’s property portfolio. Then, they spun off a large division of their enclosed shopping centres (including Orchard Park Shopping Centre). Those properties now trade as Primaris REIT (listed on the TSE under PMZ.UN). As a result, H&R’s results weren’t “normalized.”

Also, Allied Properties REIT – which focuses on Office properties had occupancies dip below 90%. Not everyone is in a hurry to return to the office. But, Allied’s brick and beam properties appeal to younger professionals – especially in the digital, high tech and telecommunications sectors. They’re desirable locations to work and they should start to see occupancies return closer to capacity.

Hence, I was curious. Given that most operating results have been “normalized,” how was the marketplace valuing these REITs compared to their book value /unit – a figure that’s meant to represent current or fair market value (FMV).

The table below lists the results of my inquiry. On Wednesday, May 18, all of our REITs were all selling below book value. Theoretically, the properties could be sold into the market place and unit holders would realize a gain on the difference between the REITs unit price and the underlying assets. In some instances, those discounts were 30% or more. An unweighted average suggests the top ten holdings are selling about 20% below their fair market price in aggregate.

I’ve also included their debt ratios as a means of gaging how leveraged they are (higher debt levels erode unitholders’ equity during downturns). Most are conservatively financed with debt ratios ranging between 21.5% of assets (Granite) and 46% of assets (Smartcentres).

In his book, The Intelligent Investor, Ben Graham talks about 2 concepts central to his approach to investing. The first is the idea of “intrinsic value.” He suggests investing (not speculating or trading) should involve independently reviewing the business attributes of a securities issue (i.e. future cash flows, etc.) and assigning a value to that enterprise. That value might ultimately represent what a prudent or reasonable person would pay for the property or business in a private business transaction.

Then, recognizing that errors could be made with assumptions, calculations, etc., one should leave a “margin of safety” prior to committing capital. By buying at a discount to intrinsic value (i.e. a margin of safety) an investor helps to protect against downside and a permanent capital loss. It’s how one preserves capital.

It’s impossible to predict what the capital and real estate markets will do over the short term, but for patient, long term investors, a portfolio of REITs might represent a solid opportunity to enhance your and your family’s wealth.

Further Reading

What You Can Learn from My Real Estate Investments by Warren Buffett. Published in the February 24, 2014, edition of Fortune magazine. If you can’t access the article, it can also be found on page 17 of the 2013 Berkshire Hathaway Annual Report under “Some Thoughts About Investing.”