Ontario’s Golden Horseshoe is one of North America’s fastest growing cities. N

In 2006, Ontario adapted the GNG project. This video explores the development of Toronto and surrounding municipalities.

In 2006, Ontario adapted the GNG project. This video explores the development of Toronto and surrounding municipalities.

Happy to present an updated due diligence video on Rio-Can Real Estate Investment Trust. Rio-Can is one of Canada’s largest commercial landlords. Units of the trust can currently be purchased at a discount to NAV (net asset value). Rio-Can REIT closed today at $22.83 /unit on the Toronto Exchange (REI.UN). That ‘s about a 12% discount to book value of $25.90 as reported at the end of Q3-22.

Their future looks bright and there best days are still yet to come. It’s a good deal.

Real estate investors can go at it alone developing projects – completing zoning applications, appeasing bankers, paying for legal work, etc. Or, they can purchase units, become unitholders of Rio-Can, own a pro-rata share in some of the best placed properties in the country and ride on the coat tails of some of the country’s top real estate minds.

Rio-Can is a latter day Little Engine that Could.

Just completed The Intelligent REIT Investor by Brad Thomas. Sorry I didn’t get to it sooner.

Thomas has written a book that combines the thinking of two legendary investors:

1) Ben Graham – author of Security Analysis, The Interpretation of Financial Statements and the Intelligent Investor and the Columbia Business Professor who mentored Warren Buffett, and

2) Ralph L. Block – longtime proponent of REITs (real estate investment trusts) and author of Investing in REITs

Ben Graham revolutionized the investment industry by suggesting long-term investors take a business approach when assessing the value and potential growth of stock and bond securities. For him, that meant paying attention to fundamentals like earnings and earnings growth, purchase price and a number of profitability ratios.

Graham never addressed REITs in his classic investing book because they’re a more recent phenomena (i.e. modern REIT legislation was established in the 1990s).

Henry Block wrote his definitive book on REITS in 2002. In his book, “Investing in REITs,” Block introduced readers to REIT structures, types of REITs (residential, industrial, etc.) and how to decipher the balance sheet (why do we use FFO to gage REIT performance vs. Net Income?). That book was written two decades ago.

Thomas’ book does a wonderful job of combining the wisdom of both these authors and updating readers with more recent trends. Technology has radically changed the nature of home and office properties over the past twenty years and Thomas does a commendable job of leading the reader through the changes.

Highly recommended for real investors.

In this video published today on YouTube, I review the latest Q3-22 operating results from Allied Properties Real Estate Investment Trust. The Business is coping in a tough office environment and currently available at some compelling valuations.

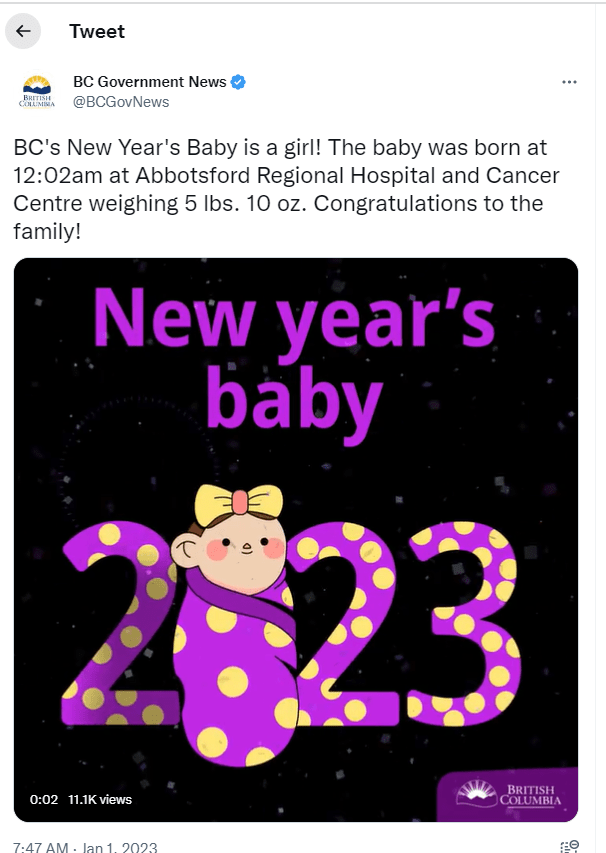

According to BC Government News, the first child born in BC was delivered at 12:02 Sunday morning at Abbotsford Regional Hospital to parents Arben Camayan and Thea Villaneuva..

Little Gabriella Louise V. Camayang weighed 5 pounds, 10 ounces (2.5 kilograms) at the time of her arrival.

A baby boy was born in Nanaimo Regional Hospital not long after. He was delivered at 12:15 and weighed 7 pounds, 10 ounces (3.45 kilograms).

BC gamblers can’t place bets on the sex or size of the babies, but they can place bets on which hospital will deliver the first New Year’s Baby through the BC Lottery Corporation. There were twenty-three potential hospitals from which to choose. Players could win $10 for every $1 wagered if they guess correctly.

The odds-on favourite was B.C. Women’s Hospital in Vancouver at 3.50. Surrey Memorial Hospital was pegged at 5.00. Royal Columbian Hospital in New Westminster, which had the province’s first baby in 2019 and 2020, marked in at 8.00.

Cowichan District Hospital and St. Joseph’s in Comox were presented the worst odds, at 50.00. while Nanaimo was at 31.00.

IF they really wish to win big, parents and grandparents should consider starting an RESP for newborns or at least as early as possible. Newborn’s accounts can benefit from time, grants, compounding and future opportunities.

Here’s how it works…

For every dollar a parent contributes to an RESP, the federal government will kick in another 20 cents through the Canada Education Savings Grant (CESG). Each $1.00 contributed quickly becomes $1.20 working and growing towards your child’s education goal.

Further, between the ages of 6-9, the BC Government will make a one-time contribution of $1,000 through the BC Training and Education Savings Grant (BCTESG).

And, for households with less than $50,000 /year of income, the Federal Government will add an additional $500 through the Canada Learning Bond (CLB) and subsequent grants based on need.

There are some limits. The CESG maxes out at $500 per year and $7,200 per child per lifetime, but that means contributing $2,500 /year or $36,000 before the beneficiary turns 17.

Parents and/or grandparents allotting $1,000 early and contributing $100/month for eighteen years will see those funds grow to: $43,000.00 – assuming a 6% compounded growth rate or $50,000.00 assuming an 8% compounded annual rate of return.

For parents and grandparents wanting to invest in their newborn’s future, there are two steps needing to be taken. First, parents will need to find an advisor or a financial institution that offers RESPs. Second, parents will need to apply for a Social Insurance Number for their infant (required for when the student withdraws funds from the account). Click here: https://www.canada.ca/en/employment-social-development/services/sin/apply.html

Betting on your child’s future is one of the best bets a person can make.

Last week, Canadian Lawyer magazine reported business insolvency filings were up 1/3 over the same quarter last year. That’s the highest year over year increase in 31 years (i.e. since 1991). Bankruptcy filings are regulated and recorded by the Office of the Superintendent of Bankruptcy

By now, most COVID restrictions have been lifted, but so have the government support programs. That means businesses (and individuals) are on their own. Expect some hiccups as they adjust to the new realities like supply chain re-alignments, staffing and product shortages, a war in Ukraine, etc.

“With inflation now at a 30-year high, the conditions are ripe for further business insolvencies. Business owners and inhouse counsel should prepare by consulting with an insolvency professional as early as possible” said Jean-Daniel Breton, chair of the Canadian Association of Insolvency and Restructuring Professionals.

Those business owners who are susceptible to economic shifts should consider holding some or all of their financial assets with an insurance company. Provided their structured properly, assets held with an insurer (i.e. in an insurance contract) are typically exempt from creditors. That’s because government and the law decided long ago that “insurance” is a societal good. Most common law provinces are on side with the exemption.

In February 1996, the Supreme Court decided a landmark case in Royal Bank vs. North American Life Assurance Co. The case surfaced because a doctor in Saskatoon fell on hard times and couldn’t pay his rent. The landlord sued and the doctor declared bankruptcy. When creditors attempted to seize registered (RRSP) assets that were held with North American Life Insurance company, the Saskatchewan court “exempted” these assets. The case was appealed by the Royal Bank of Canada all the way to the supreme court (seems lenders don’t like the idea of some assets being exempted – especially by life insurance companies).

In their ruling, the Supreme Court of Canada based their conclusion on three critical issues:

#1 – The assets in question were governed by provincial Life Insurance legislation.

#2 – The owner had designated a preferred class of beneficiary (i.e. family member).

#3 – There was NO evidence of a “fraudulent conveyance.”

Viewers may want to view this You-Tube video…

If you understood a business perfectly and the future of the business, you would need very little in the way of a margin of safety. SO, the more vulnerable the business is, assuming you still want to invest in it, the larger margin of safety you’d need. IF you’re driving a truck across a bridge that says it holds 10,000 pounds and you’ve got a 9,800 pound vehicle, if the bridge is 6 inches about the crevice it covers, you may feel okay, but if it’s over the Grand Canyon, you may feel you want a little larger margin of safety.”

Warren Buffett, 1997 Berkshire AGM

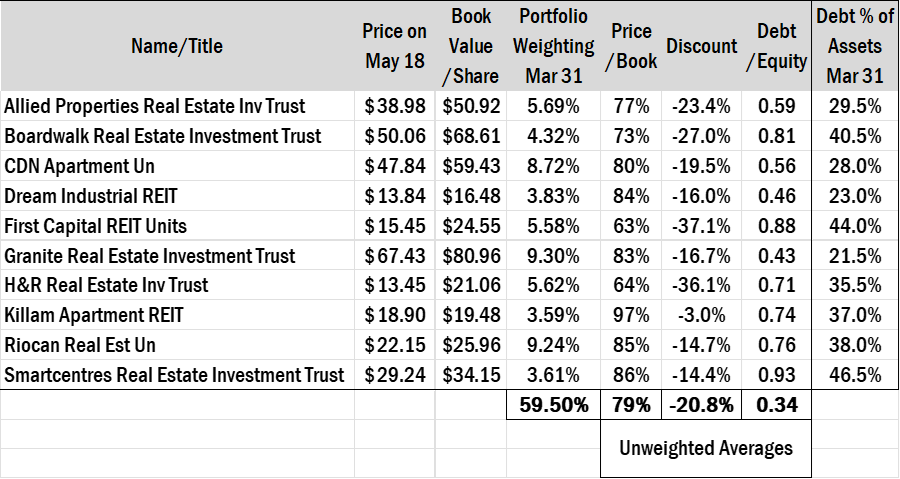

Over the past few days, I’ve been posting the first quarter operating results of top ten REITs from our property portfolio.

Most of the REITs have reported satisfactory results. They’ve all survived the pandemic and now they’re emerging as expected. Revenues, Net Income, FFO (Funds from Operations), SPNOI (Same Property Net Operating Income) and Occupancies were up for the most part. Outstanding rents have been recovered. Most are proceeding with further development of their pipelines.

A couple of exceptions bear note. Figures at H&R REIT were a bit abnormal. Last Summer, H&R REIT sold the Bow to affiliates of Oak Street Real Estate Capital. “The Bow” is one of the tallest buildings in Western Canada and it was a crown jewel in H&R’s property portfolio. Then, they spun off a large division of their enclosed shopping centres (including Orchard Park Shopping Centre). Those properties now trade as Primaris REIT (listed on the TSE under PMZ.UN). As a result, H&R’s results weren’t “normalized.”

Also, Allied Properties REIT – which focuses on Office properties had occupancies dip below 90%. Not everyone is in a hurry to return to the office. But, Allied’s brick and beam properties appeal to younger professionals – especially in the digital, high tech and telecommunications sectors. They’re desirable locations to work and they should start to see occupancies return closer to capacity.

Hence, I was curious. Given that most operating results have been “normalized,” how was the marketplace valuing these REITs compared to their book value /unit – a figure that’s meant to represent current or fair market value (FMV).

The table below lists the results of my inquiry. On Wednesday, May 18, all of our REITs were all selling below book value. Theoretically, the properties could be sold into the market place and unit holders would realize a gain on the difference between the REITs unit price and the underlying assets. In some instances, those discounts were 30% or more. An unweighted average suggests the top ten holdings are selling about 20% below their fair market price in aggregate.

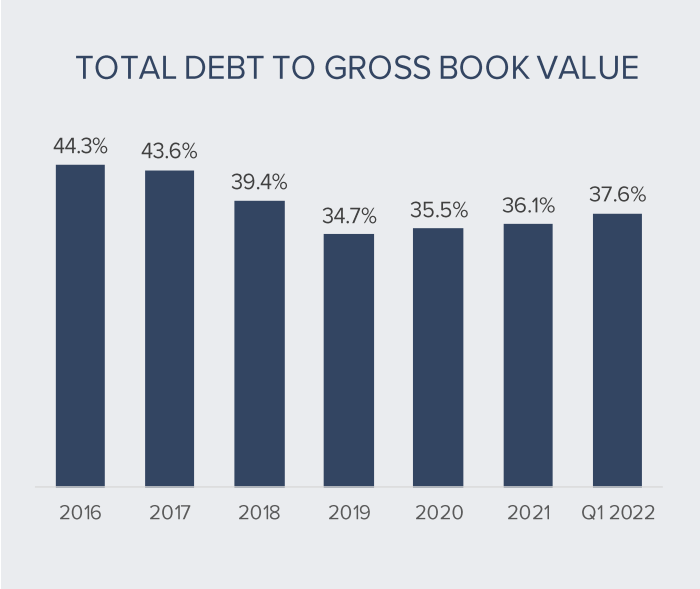

I’ve also included their debt ratios as a means of gaging how leveraged they are (higher debt levels erode unitholders’ equity during downturns). Most are conservatively financed with debt ratios ranging between 21.5% of assets (Granite) and 46% of assets (Smartcentres).

In his book, The Intelligent Investor, Ben Graham talks about 2 concepts central to his approach to investing. The first is the idea of “intrinsic value.” He suggests investing (not speculating or trading) should involve independently reviewing the business attributes of a securities issue (i.e. future cash flows, etc.) and assigning a value to that enterprise. That value might ultimately represent what a prudent or reasonable person would pay for the property or business in a private business transaction.

Then, recognizing that errors could be made with assumptions, calculations, etc., one should leave a “margin of safety” prior to committing capital. By buying at a discount to intrinsic value (i.e. a margin of safety) an investor helps to protect against downside and a permanent capital loss. It’s how one preserves capital.

It’s impossible to predict what the capital and real estate markets will do over the short term, but for patient, long term investors, a portfolio of REITs might represent a solid opportunity to enhance your and your family’s wealth.

What You Can Learn from My Real Estate Investments by Warren Buffett. Published in the February 24, 2014, edition of Fortune magazine. If you can’t access the article, it can also be found on page 17 of the 2013 Berkshire Hathaway Annual Report under “Some Thoughts About Investing.”

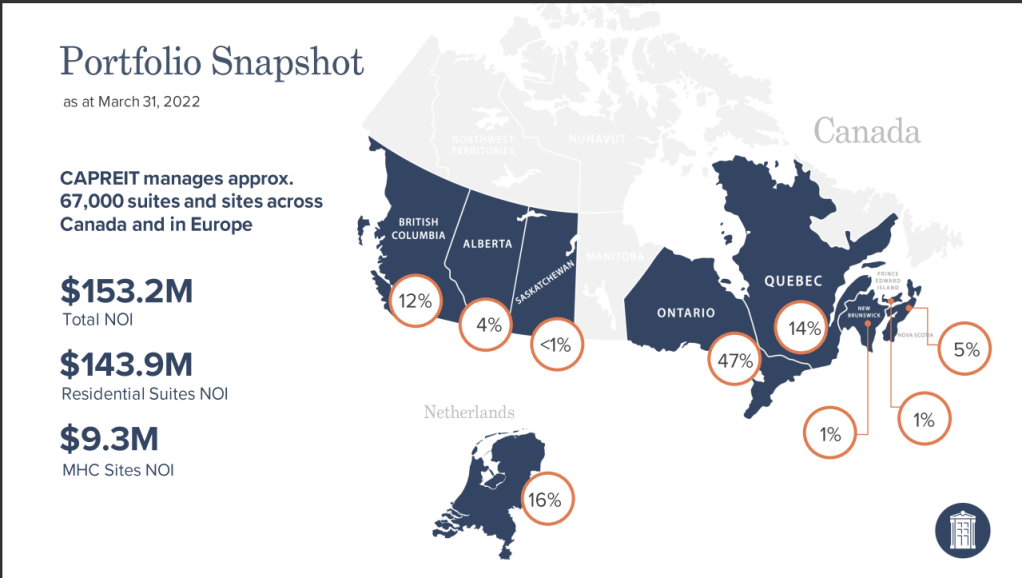

On May 17-2022, Canadian Apartment REITs published their first quarter business results. They are the last of our property portfolio “partners” to report.

In addition to being the largest residential REIT and one of the largest holdings in our real estate portfolio, CAP REIT is also the largest landlord in Canada. Their operations are a fairly telling bell weather of the residential real estate business in Canada.

As of March 31, 2022, they reported the following results:

“Following another strong and accretive year in 2021, we continued to generate solid growth and strong operating performance in the first quarter of 2022. Occupancies rose to 98.0% at March 31, 2022, up from 97.3% at the same time last year while average monthly rents increased 3.9%. Importantly, our balance sheet and financial position remained strong and resilient with a significant liquidity position.”

“Total operating revenues increased 8.4%, driven by the contribution from acquisitions completed over the last twelve months, increased stable occupancies and higher average monthly rents. Total property Net Operating Income (“NOI”) rose 4.4% compared to the same period last year. Stabilized property NOI decreased slightly in the quarter due increased weather-related maintenance costs, higher utilities costs resulting from the colder winter this year and a significant increase in the cost of natural gas, and higher property taxes. Importantly, to date we have collected over 99% of our rents, a testament to our successful initiatives to work with our residents and understand their issues through the pandemic.

During 2021, we acquired 3,744 apartment suites, townhomes and manufactured housing community sites in Canada and the Netherlands for total costs of approximately $1.05 billion. In the first three months of 2022, we further expanded our property portfolio with the purchase of 1,015 suites and sites for total costs of $439million[1]. These new properties will make a strong, accretive and growing contribution in the months and years ahead. Looking ahead, while our acquisition pipeline remains strong and robust, we will also be examining our total portfolio to determine opportunities to generate value for our Unitholders and additional capital to fund more accretive growth opportunities.”

Further information about CAP REITs financials can be found by clicking here: https://s25.q4cdn.com/722916301/files/doc_financials/2022/q1/Q1-22-Full-Report.pdf

Their most recent presentation to investors can be viewed here: https://s25.q4cdn.com/722916301/files/doc_financials/2022/q1/Q1-2022-CC-Slides-(FINAL).pdf

[1] Average cost per (apartment) units purchased in Q1-2022 was approx. $432,512.31. Average cost per units purchased in 2021 was $280,448.71. That amount includes the purchase of “townhomes and MHCs,” which would explain the lower average suite cost.

This Post is published on or around May 17th, 2022, and it includes timely information that can be quickly rendered obsolete. It is FOR INFORMATION PURPOSES and simply meant to keep partners informed about some of the holdings in our portfolios. This is NOT an OFFER to purchase securities or products & NO representation is being made. Items presented may NOT be suitable for everyone. Rates change. Values will fluctuate. Please consult an experienced, qualified, licensed professional prior to investing and ensure that your investments are a part of a comprehensive plan designed to help you & your family meet your long-term financial goals & objectives.

Gordon Wiebe is registered as a “Life, Accident & Sickness” insurance underwriter with the Insurance Council of B.C, the Alberta Insurance Council & the Saskatchewan.