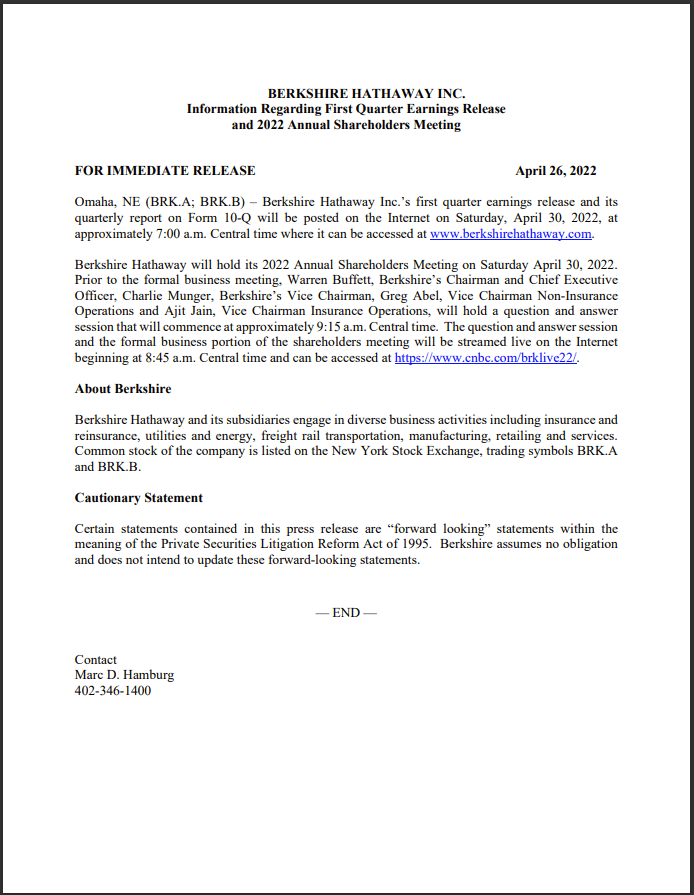

We are now less than 48 hours away from the 2022 Berkshire Hathaway Annual Meeting, aka “the Woodstock for Capitalists.” The meeting begins Saturday morning at 6:45 am (pacific) 8:45 (central) and it can be viewed by clicking this link: https://www.cnbc.com/brklive22/

I regret I won’t be traveling to Omaha this year. I’ve been to several meetings since 2001 and the Berkshire AGM is always a fun event. In addition to hearing Warren Buffett and Charlie Munger live, there are countless events happening around town (Nebraska Furniture Mart Bar-B-Cue), the Friday night Borsheim’s reception, etc.

Then, there are the “Berkshire company” displays and booths in the exhibit hall offering shareholders tremendous value on everything from boxer shorts (Fruit of the Loom) to gourmet chocolates (See’s Candies), kitchen utensils (Pampered Chef), air compressors (Campbell Hausfield), car insurance (GEICO), Buffett Books (the Book Worm), cowboy boots (Justin Brands) and luxury manufactured homes (Clayton homes). It’s festive and the booths are staffed by midwestern sales staff who know their craft.

You never know who you’re going to see. “That’s Bill Gates eating a Dilly Bar.” “That’s Susan Lucci buying jewelry at Borsheim’s.” “That’s Bill Ackman at the microphone.” “That’s Lou Simpson…” RIP

There are receptions hosted by other reputable investors and Berkshire disciples including the Markel brunch reception at the Marriott on Sunday morning. See: https://youtu.be/F_OnccXU8ZU One of these years I will have the pleasure of meeting Tom Gayner – the Markel sage from Richmond, VA.

Whitney Tilson will host his annual cocktail reception on Friday night https://www.eventbrite.com/e/whitney-tilsons-cocktail-party-before-the-berkshire-hathaway-annual-mtg-tickets-308282921517

This AGM will be the first since 2019. The COVID pandemic prevented a live event in 2020 and 2021. I suspect regular attendees will be happy to see everyone again.

If you’re not able to attend, you can still get yourself out of bed this Saturday morning and hear two of the world’s brightest investment minds.

More information, visit the Berkshire https://www.berkshirehathaway.com/news/apr2622.pdf