Tom Gayner once commented that the secret to investing successfully is surviving the first thirty years. He was half joking and half serious, but his reasoning was sound. He suggested, after that length of time an investor would have experienced several market trends and cycles and he ought to be able to recognize their recurrence.

Since the new year, market participants have seen the following:

- a hike in interest rates

- a 13.5% decline in the S&P 500

- a 9.5% decline in the Dow Jones Industrial Average (DJIA)

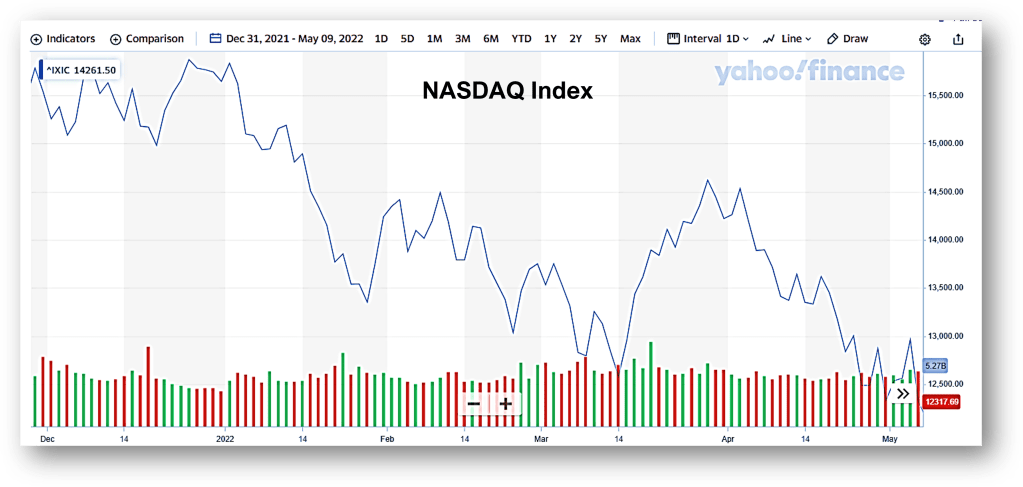

- a 25% decline in the NASDAQ

None of these should come as a surprise to anyone. As Yogi Berra might say, “IT’s déjà vu all over again.”

In January 1966, the Dow Jones Industrial Average hovered around 8,891. But, by June 1982 – after years of decline, the DJIA had surrendered 72% of its value closing around 2,406. “The Nifty Fifty” – a group of cutting-edge, high-tech companies including Xerox, Polaroid, Kodak, etc. had vaulted the DJIA to lofty levels. It seems speculators were willing to pay 50-100 times earnings – not unlike some of the valuations we’ve seen in the recent market environment.

The late 1990’s also saw similar valuations placed upon countless dot.com/high tech companies as the world prepared for Y2K.

When speculation ramps up, it can drive equities to levels that simply aren’t sustainable or justifiable. Is it any wonder the NASDAQ has lost 25 percent so far this year?

Investors and speculators seeking refuge in fixed income won’t find much comfort either. If interest rates continue to rise – as they’re likely to do, bond valuations will also decline.

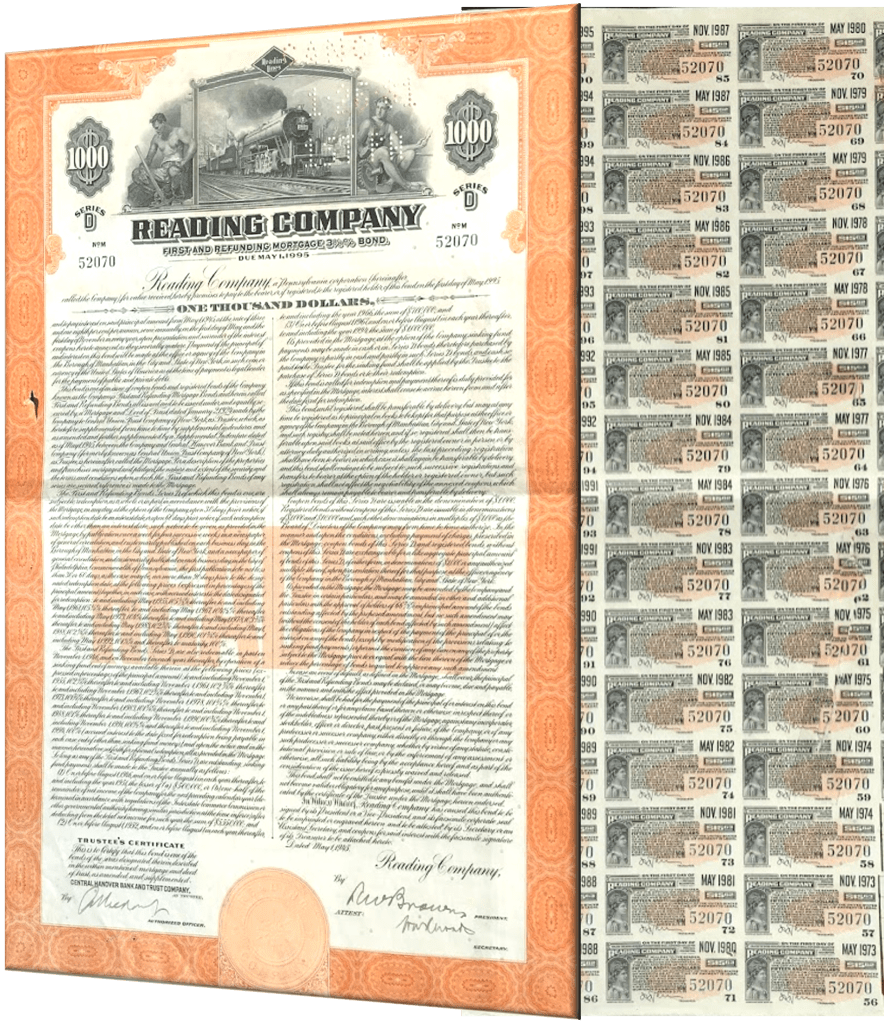

As a reminder of this, I keep a de-commissioned “50-year bond” certificate on my wall. The bond was issued in 1945 by the Reading Railroad Co. (yes, the same one from Monopoly). The bond was set to mature in 1995 and the attached coupons paid an annual rate of 3.25%.

In 1972, the bond was surrendered. The owner would have likely seen a 40% drop in the value of the bond as interest rates climbed from 5.45% in March 1972 to 6.66% in July.

It’s impossible to know what interest rates or markets will do over the short term. There are advantages to be had by studying market history and those of us over 55, have been to this rodeo before.