Nearly all the REITs held in our Real Estate investment contracts have reported their first quarter earnings. Canadian Apartment REIT reports tomorrow.

Normally, one shouldn’t attach too much significance to quarterly earnings as it can take years for the value of great properties and enterprises to be realized. Nevertheless, operating results for the first quarter are presented here as an indicator of how business operations are unfolding as the REITs and economy emerge from pandemic restrictions.

Overall, revenues, income, funds from operations (FFO), occupancies have improved significantly. CAP REIT reports tomorrow. Rio-Can figures reported in an earlier blog and can be viewed here: https://think-income.com/2022/05/11/getting-it-reit/

On April 27, Allied Properties REIT reported the following:

“Allied’s first-quarter results for 2022 met or exceeded expectations, with AFFO per unit and average in-place net rent per occupied square foot rising to record levels,” said Michael Emory, President & CEO. “FFO per unit was 61 cents and AFFO per unit 56 cents, up from the comparable quarter last year by 4% and 7%, respectively. NAV per unit at quarter-end was $50.92, up from the end of the first quarter last year by 5% and up from the end of 2021 by 1%. Leasing activity continued to accelerate through the quarter, with average in-place net rent per occupied square foot rising to $25.13, up from the comparable quarter last year by 4% and up from the end of 2021 by 2%.”

On May 9th, Boardwalk posted their quarterly results. Chairman & CEO Sam Kolias reported:

“We are pleased to report on another solid quarter to begin 2022, with growth in NOI, FFO, and Profit through the Omicron wave of the pandemic and non-controllable cost inflation primarily in our utilities expense through the winter months. As we look forward to our busy spring and summer leasing season, we have seen significant leasing gains with our May occupancy increasing to 96.6%. Leasing spreads on both renewals and new leases have seen strong improvement, and in our largest market of Alberta, have seen renewal spreads increase to 4.7% in the month of April. New lease spreads have also turned positive with housing fundamentals improving in each of our markets allowing for incentive reductions and positive rental rate growth.”

On May 3rd, Dream Industrial reported net income of $442.9 million in Q1 2022, a 364.9% increase when compared to $95.3 million in Q1 2021. The increase was primarily due to increases in fair value adjustments to investment properties (NOTE: companies are required to include unrealized gains in the value of assets as a part of earnings).

Net rental income was $65.3 million in Q1 2022, a 40.0% increase when compared to $46.7 million in Q1 2021. Year-over-year net rental income growth was primarily driven by 38.8%, 46.5% and 264.9% increases in Ontario, Québec and Europe, respectively.

Diluted funds from operations (“FFO”) per Unit were $0.22 in Q1 2022, a 16.0% increase when compared to Q1 2021, where the diluted FFO per Unit were $0.19.

• Total assets were $6.7 billion in Q1 2022, a 10.8% increase when compared to $6.1 billion in Q4 2021;

• Net asset value (“NAV”) per Unit was $16.48 in Q1 2022.

For the three months ended March 31, 2022, First Capital recognized net income attributable to Unitholders of $44.5 million or $0.20 per diluted unit compared to $38.0 million or $0.17 per unit for the same prior year period. The increase was primarily due to an increase in the fair value of investment property of $8.8 million.

FFO per unit remained unchanged primarily due to a $3.1 million increase in interest and other income, and interest expense savings of $2.8 million, which were offset by other losses primarily related to unrealized losses on marketable securities, totaling $6.8 million, or $0.03 per unit.

SPNOI – Same Property NOI Growth increased 1.9%, despite a 20 basis point decline in occupancy. The growth was primarily due to a $2.2 million decrease in bad debt expense as well as rent escalations, partially offset by lower occupancy and a $0.6 million decrease in lease termination fees over the prior year period.

Portfolio Occupancy: March 31, 2022 portfolio occupancy of 95.5% decreased 0.6% on a quarter-over-quarter basis from 96.1% at December 31, 2021 primarily due to net closures (which primarily related to closures for redevelopment). On a year-over-year basis, total portfolio occupancy declined 0.3% from 95.8% at March 31, 2021 to 95.5% at March 31, 2022.

Granite’s net operating income (“NOI”) was $91.2 million in the first quarter of 2022 compared to $81.5 million in the prior year period, an increase of $9.7 million primarily as a result of net acquisition activity beginning in the first quarter of 2021;

• Same property NOI (Net Operating Income) or SPNOI – cash basis increased by 4.6% for the three-month period ended March 31, 2022.

• Funds from operations (“FFO”)(1) were $69.4 million ($1.05 per unit) in the first quarter of 2022 compared to $57.1 million ($0.93 per unit) in the first quarter of 2021.

• Granite recognized $490.6 million in net fair value gains on investment properties in the first quarter of 2022 which were attributable to various factors including fair market rent 1 increases as well as compression in discount and terminal capitalization rates for properties located in the GTA, the United States and Europe. The value of investment properties was partially offset by unrealized foreign exchange losses of $146.1 million resulting from the relative strengthening of the Canadian dollar against the US dollar and

• Granite’s net income attributable to stapled unitholders increased to $497.7 million in the first quarter of 2022 from $230.1 million in the prior year period primarily due to a $281.1 million increase in net fair value gains on investment properties and a $9.7 million increase in net operating income as noted above, partially offset by a $30.6 million increase in deferred tax expense

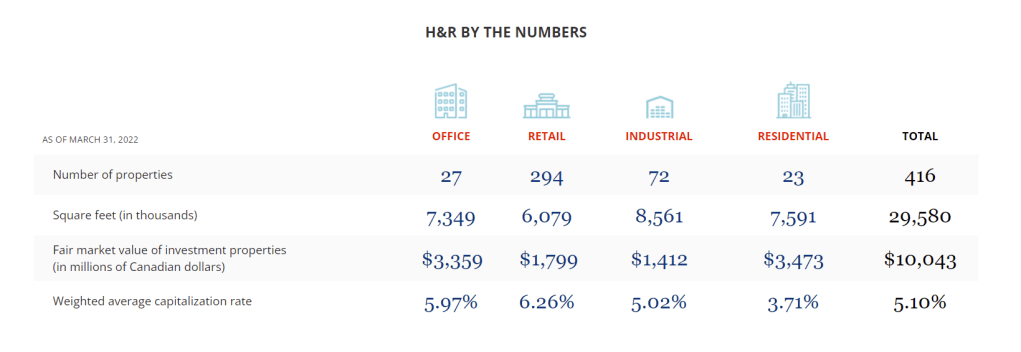

On May 12, 2022, H&R Real Estate Investment Trust (“H&R” or “the REIT”) (TSX: HR.UN) reported the following operating results:

“Our strong first quarter financial results mark a pivotal moment in the continuation of our transformation and the surfacing of the embedded value within our portfolio,” said Tom Hofstedter, CEO. “Following the successful spin out of our enclosed shopping centre division (i.e. Primaris) and the sale of the Bow and Bell office campus, our portfolio today is significantly more concentrated on higher growth asset classes within strong urban markets. Today’s results are a testament to the quality of our properties, platform and strategic plan.”

Highlights

30.9% decrease in net operating income as compared to Q1-2021 primarily due to the spin‐off of Primaris REIT and property dispositions throughout 2021;

$19.88 unitholders’ equity per Unit, an increase of $3.33 from December 31, 2021;

$21.06 Net Asset Value (“NAV”) per Unit(2), an increase of $3.36 from December 31, 2021;

Sold 33.3% non‐managing interest in The Pearl, in Austin, Texas for approximately U.S. $45.8 million, generating a gain of $20.7 million over construction cost, and a return on equity invested of approximately 221.5%;

13,715,500 Units repurchased year to date, at a weighted average price of $12.97 per Unit, for a total cost of $177.8 million as at May 10, 2022;

19.1% Same‐Property net operating income (SPNOI) (cash basis)(1) growth driven by strong residential and office rental growth together with industrial and retail property lease‐ups

“Killam’s first quarter earnings growth and operating performance were strong,” noted Philip Fraser, President and CEO. “The same property revenue growth of 5.1% in Q1-2022 reflects the strong demand for housing across all our markets. Despite a colder winter season and higher heating costs this quarter, Killam achieved 3.1% same property net operating income growth to start the year.”

Killam earned net income of $60.0 million in Q1-2022, compared to $27.4 million in Q1-2021. The increase in net income is primarily attributable to fair value gains on investment properties, growth through acquisitions, completed developments, and increased earnings from the existing portfolio.

Killam generated FFO per unit of $0.24 in Q1-2022, a 4.3% increase from $0.23 per unit in Q1-2021. AFFO per unit increased 5.3% to $0.20, compared to $0.19 in Q1-2021. The growth in FFO and AFFO was primarily attributable to increased NOI from Killam’s same property portfolio and incremental contributions from over $400 million in recent acquisitions. This growth was partially offset by a 9.4% increase in the weighted average number of units outstanding.

Despite inflationary pressures, Killam achieved 3.1% growth in same property consolidated NOI during the quarter. This improvement was driven by 5.1% growth in revenue, partially offset by an 8.2% increase in operating expenses.

On May 11, SmartCentres REIT reported, “substantive improvement in retail leasing momentum across the portfolio with growth from both existing and new tenants;”

Highlights:

Progress in zoning approvals on strategic projects, together with improved market conditions, contributed to $237.7 million in incremental property values, leading to net income and comprehensive income for Q1 2022 increasing to $370.1 million compared to $60.6 million for the same period in 2021; from an increase of $1.71 per Unit;

FFO per Unit(1) for Q1 2022 increased by $0.02 or 4.1% as compared to the same period in 2021;

Total unencumbered assets(1) increased from $5.9 billion at March 31, 2021 to $8.4 billion at quarter end; and

Continued advancement of non-retail pipeline of 283 projects representing approximately 59 million square feet across the network (41 million square feet at the Trust’s share)

Of the top 0.1 percent of wage earners in America – those earning $1.48 million per year, most of them draw income from owning a regional supply business like an auto dealership or a beverage distribution company. Yes, there are celebrities, actors and athletes who make piles of money given their talent and notoriety, but three times as many affluent taxpayers make the majority of their income from business ownership. Salaries don’t make people rich nearly as often as equity does.

The nature of those businesses tends to be dull and boring including: auto repair shops, gas stations, business equipment contractors, etc. Their businesses tend to endure because they provide goods and services that meet long term needs and demands. This tends contrasts “sexy” businesses like salons, cosmetic stores, record stores, and clothing stores. These “sexy” businesses have a limited life expectancy. On average, they typically fold after 2½ – 4 years.

Another important feature of their businesses is their ability to avoid ruthless price competition – either through a monopoly or a regional advantage, etc. For instance, more than 20 percent of auto dealerships in America have an owner making more than $1.58 million per year. Those dealerships have legal protections; state franchising laws that give auto dealers exclusive rights to sell cars in a territory. Same for many beverage distributors, which act as middlemen between alcohol companies and stores and supermarkets.

The advantages of business equity isn’t lost on the owners. Most of them are happy to maintain the status quo. Turnover is minimal (i.e. don’t be looking to purchase one of these businesses at a discount anytime soon).

The author then asks, “If pop culture is right in suggesting getting rich is a path to happiness?” I’ll examine that in a subsequent blog. For now, I’m going to see if I can find a cheap distribution business.

About the Author:

Seth Stephens-Davidowitz graduated from Harvard in 2013 with a PhD inEconomics. His work has focused on using big data sources to research behaviours and attitudes. Using “big data” sources, his essay explores who are the rich in America and what relationship wealth plays in happiness (not for the faint of heart).

The Well in Toronto is Canada’s Largest Development ever. It’s Being Managed by RioCan & Allied REITs.

If anyone needed further evidence showing how uncorrelated a company’s share price (or a REIT’s unit price) can be from its underlying value, RioCan (REI.UN) provided a good example yesterday.

Net income of $160.1 million, exceeding the comparable period last year by $53.3 million

FFO (Funds from Operations) of $0.42 /unit, up 27% year of year (YoY)

A 4.1% increase in SPNOI – Same Property Net Operating Income

1.1 million sq. ft. of new and renewed leases

Occupancy was 97% – up to pre-pandemic levels

42.6 million ft2 in the “development pipeline”

16.8 million ft2 of zoning approved

2.2 million ft2 under construction

2.5 million ft2 “shovel ready”

3.2 million ft2 actively being “redeveloped”

1.7 million ft2 expected to be delivered in the next 24 months

27.4 million of new funds expected in 2022

Weighted interest costs are at 2.98%

Book Value /unit $25.96 as of March 31, 2022.

Most landlords would be satisfied with those quarterly results. So, how did the market respond to their business operations? The unit price dropped $1.15 or 5% to $20.65 from $21.80 and then closed at $20.99. It was one of the most traded issues on the Toronto Stock Exchange.

RioCanowns and operates 204 premier retail properties in Canada. They lease over 36 million square feet of space and their enterprise value is roughly $15 billion.

At $21 /unit, an investor can purchase a pro-rata interest at a discount of 19%.

As with the Berkshire Hathaway AGM, Markel management places a premium on relationships and personal attendance. I haven’t found anything that suggests the meeting and/or panel discussions will be webcast. I will post links if I do.

I’ve been a Markel shareholder and a Tom Gayner for years, but have yet to make the trek to Richmond, VA. My planned trip in Spring 2020 was cancelled due to COVID.

“Markel Re-Affirms Commitment to Renewable Energy,” March 24, 2022. Tom Baker, Markel’s International Head of Renewable Energy, discusses 2021 achievements in the renewable energy market and what’s ahead in 2022.

“Markel’s 2021 Corporate Giving” February 23, 2022. Honoring its commitment to community, Markel achieved another historic year of corporate giving in 2021 across its insurance group.

“Morgen Housel Joins Markel’s Board of Directors” Honoring its commitment to community, Markel achieved another historic year of corporate giving in 2021 across its insurance group. November 16, 2021.

Further Reference…

The Evolution of a Value Investor – Talks at Google – June 22, 2015. Tom Gayner is the CIO of Markel Corp, where he manages the company’s investment portfolio. He talks about his journey as an individual and value investor. A recent Wall Street Journal feature on Mr Gayner’s investing style mentions: ‘He has an outstanding investing record. He works only for Markel and doesn’t take outside clients, but every investor can learn from him.’ You never woul’ know any of this [extraordinary success] from listening to Mr. Gayner. After a good year, most portfolio managers beat their chests even harder than they beat the market; Mr. Gayner’s 2014 report merely said, “our overall equity portfolio earned 18.6%,” without even mentioning that the S&P 500 was up 13.7%. Instead of trying to mimic the inimitable brilliance of Mr. Buffett, maybe more investors should emulate the common sense and patience of Mr. Gayner.“

Tom Gayner once commented that the secret to investing successfully is surviving the first thirty years. He was half joking and half serious, but his reasoning was sound. He suggested, after that length of time an investor would have experienced several market trends and cycles and he ought to be able to recognize their recurrence.

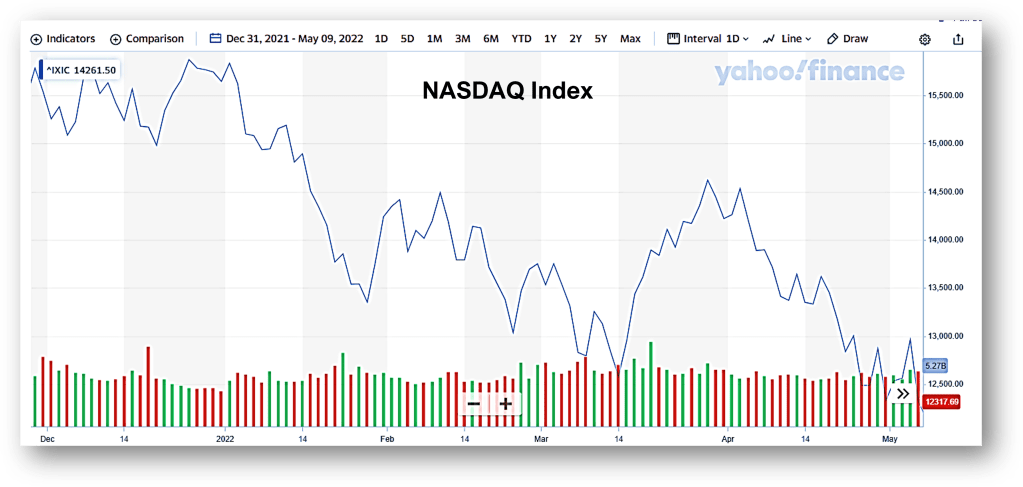

Since the new year, market participants have seen the following:

a hike in interest rates

a 13.5% decline in the S&P 500

a 9.5% decline in the Dow Jones Industrial Average (DJIA)

a 25% decline in the NASDAQ

None of these should come as a surprise to anyone. As Yogi Berra might say, “IT’s déjà vu all over again.”

In January 1966, the Dow Jones Industrial Average hovered around 8,891. But, by June 1982 – after years of decline, the DJIA had surrendered 72% of its value closing around 2,406. “The Nifty Fifty” – a group of cutting-edge, high-tech companies including Xerox, Polaroid, Kodak, etc. had vaulted the DJIA to lofty levels. It seems speculators were willing to pay 50-100 times earnings – not unlike some of the valuations we’ve seen in the recent market environment.

The late 1990’s also saw similar valuations placed upon countless dot.com/high tech companies as the world prepared for Y2K.

When speculation ramps up, it can drive equities to levels that simply aren’t sustainable or justifiable. Is it any wonder the NASDAQ has lost 25 percent so far this year?

Investors and speculators seeking refuge in fixed income won’t find much comfort either. If interest rates continue to rise – as they’re likely to do, bond valuations will also decline.

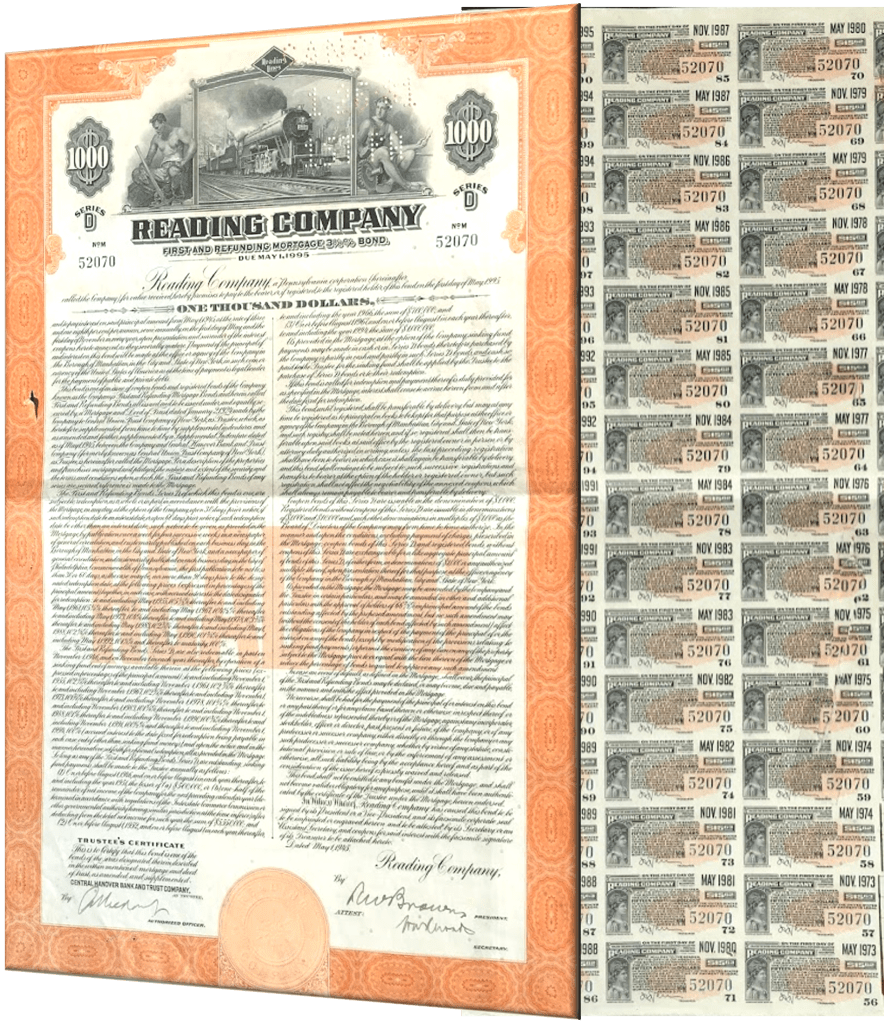

As a reminder of this, I keep a de-commissioned “50-year bond” certificate on my wall. The bond was issued in 1945 by the Reading Railroad Co. (yes, the same one from Monopoly). The bond was set to mature in 1995 and the attached coupons paid an annual rate of 3.25%.

In 1972, the bond was surrendered. The owner would have likely seen a 40% drop in the value of the bond as interest rates climbed from 5.45% in March 1972 to 6.66% in July.

It’s impossible to know what interest rates or markets will do over the short term. There are advantages to be had by studying market history and those of us over 55, have been to this rodeo before.

Research suggests many of them used their home equity to acquire HELOCs (Home Equity Lines of Credit). Then, they leveraged the HELOCs to secure a down payment while financing the rest of the real estate purchase with a traditional mortgage (NOTE: in Canada, real estate investors must commit 20% of the property value but can finance the rest with a traditional mortgage).

Interest rates on HELOCs float with the prime rate. Borrowers are obligated to pay interest, but not principal. So, many of the investment properties would really have been financed 100% – a problem the author is wise to report on.

Studies indicate 37% of Toronto landlords are already cash flow negative

Benjamin Tal & Shaun Hildebrand – Urbanation

As interest rates rise, landlord’s carrying costs increase. Studies indicate 37% of them are already cash flow negative. Many of them will likely be inclined to raise rents in an inflationary environment. Expect some tension on that front. For the record, I’ll be siding with the tenants on this one – many of whom should have been “first time home buyers” but were sidelined as secondary parties drove up values.

Real estate investors will have bid up the price on properties betting the increase in real estate values will make up for period of negative cash flow (much like owners of NHL franchises who frequently operate at a loss, but are rewarded when they sell the franchise for a premium).

Figures from article.

But, what if values don’t continue to rise – at least over the short – medium term? How much pain can those new landlords endure? What happens if property values decline? Will they stay the course or will they dump their investments and realize losses?

There are some very real risks involved in this scenario. The outcome could be worse than anyone imagined.

This morning’s Wall Street Journal ran an editorial entitled, “Warren Buffett on Wall Street Gambling. Seems the WSJ editorial board took issue with Buffett & Munger calling out Wall Street for the way they promote “gambling” activity.” They wrote:

“Warren Buffett is apparently shocked, shocked to find gambling going on in financial markets. That was the headline from the Berkshire Hathaway CEO’s remarks at its annual meeting on Saturday in Omaha. “It’s a gambling parlor,” Mr. Buffett said, and he blamed the financial industry for encouraging risky and speculative behavior.”

That Buffett and Munger called out Wall Street for croupier like behaviour shouldn’t surprise anyone. They’ve been doing it for decades. They and value investors of all stripes have long distinguished between “investing,” “speculating” and “gambling.” It’s even the first issue addressed by Ben Graham – Buffett’s teacher and mentor in The Intelligent Investor (Chapter One, paragraph 1).

For Buffett, investing means “laying out money now with the reasonable expectation that you will receive more later.” And to further quote Ben Graham, “investing is most intelligent when it is most business like.” It’s why Buffett has always made decisions based on business fundamentals, not unbridled speculation. His focus has always been on “productive assets” and he addressed that during the meeting.

Speculation on the other hand, utilizes the “greater fool theory.” You purchase some item – tulip bulbs, pet rocks, chia pets, Netscape shares, hockey cards, cryptocurrencies, NFTs, etc. with the hope that some other fool will pay you more for that item at a later date. The item’s utility is irrelevant. These ideas haven’t changed. So, what has?

Well, a few things and they tried to address some of them.

First, Charlie noted how computer algorithms compete against other computer algorithms to make split second trades. The folly of this method stems back as far as the crash of ’87, but the computers are much quicker and far more sophisticated now. The potential for loss has increased exponentially. So has the number of people effected.

Second, neither has been impressed with Robinhood or any of the quick trade, no fee apps that surfaced during the pandemic. Platforms encouraging people to make rapid fire trades without any consideration to business fundamentals is tantamount to gambling. It’s how you turn a coveted American capitalist institution like the NYSE into a gambling parlour. It’s nothing really to aspire to. As Charlie said, “We have people who know nothing about stocks being advised by Wall Street people who understand even less. Why would you want your country’s public companies being traded like it’s a casino?”

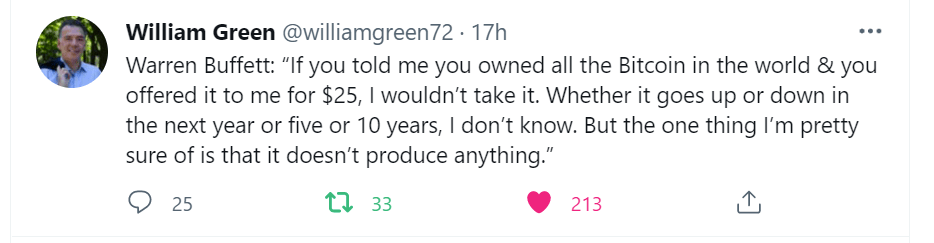

Finally, the two took aim at Bitcoin and other the cryptocurrencies. Buffett went on to explain the value of the greenback and currency that was authorized by the U.S. Federal Reserve. “Right on the bill in the lower corner it reads, “this note is legal tender for all debts, public and private.” It’s how you pay the IRS. IF you offered me all the Bitcoin in the world for $25, I wouldn’t pay it.”

The WSJ board suggested Warren and Charlie were unfairly scapegoating Wall Street and addressing symptoms vs. the actual problem. According to the board, “greed” is the real driving force and it’s not going away anytime soon as if to suggest, they’re just filling a need.

Well, that could be, but it’s not like that attitude is going to move humanity further along. I’m inclined to agree with Ben, Warren, and Charlie. Investing is most intelligent when it is most businesslike.”

BloggN from the Okanagan – Didn’t make it to Omaha this year, but happy to view the meeting live on the web from the Okanagan. What follows below are my notes from the 2022 Berkshire Hathaway Annual Meeting. It’s a work-in-progress. I’ll be reviewing and updating to ensure the script reflects more closely what was said at the meeting.

Warren: “Feeling good to be back after 3 years and actually seeing owner/partners… “Charlie and I are now combined – a 190 years old. And, I think your entitled as the owner of the company – if you have two guys, 98 and 91 running the company, you’re entitled to actually seeing them in person.”

“The new test for a business is to ask if it’s a business that could be run by a guy with Alzheimer’s.”

Introduction of Greg Abel and Ajit Jain.

AGENDA – What we’ll do today… We’ll talk about what’s happened in the last quarter and bring up a few other things you might be interested in. Then, we’ll go on to questions until noon. Break for an hour. Then, we’ll come back and we’ll take more questions until 3:30. We’ll convene the shareholders meeting at 3:45 – we’ll take a break for 15 minutes. Then, once that’s done we’ll all go our various ways.

Sales Update – 12,000 shareholders came and spent money at the exhibits from 12:00 – 5:00. We brought in eleven tons of See’s Candies – If we don’t sell out, Charlie and I get the rest. See’s set a record for sales at the Friday afternoon. Mary See is on the cover of the box. A lot of people think that’s me in drag, but that’s simply not true. There’s a certain resemblance, but… these rumors are started by our competitors. Don’t pay any attention.

That’s our schedule for the day…

The Value of Partnership – We like to give shareholders, owners, partners the same information at the same time and preferably when stock markets aren’t open. It seems to us that everyone ought to be on the same playing field… We don’t know how many shareholders we have. They’ve changed the rules over time. We can’t keep track of it like 50 years ago. We’re told by the people at Broadridge that we have 3.5 million accounts. We pay them by the accounts, but that is a lot of people that trust us.

“Trust is a Great Motivator” They rightly or overwhelmingly feel that they’re our partners. Some of them will read the financial information that we’ve given you, but a great many of them just say, “We’ve saved this money and we trust you and Charlie. And, that’s a great motivator. You’ll take care of it and I’m not going to learn accounting and try and read all those statements…”

Buffett comments about most recent10Q. “No big surprises. We prefer to use “operating earnings” – after depreciation, interest and taxes – Unlike other companies that prefer to tell you anything but what they earned. We do separate out capital gains. Over time… over the next twenty years, I would expect us to have net capital gains vs. not, but who knows? I’ll report to you in twenty years whether or not that’s the case. We made about $7 billion during the first quarter. That’s real $7 billion. Basically have that in cash when the quarter is over. We’re talking $7 billion of real money and those managers who you were in the movie… they’re the people who work with your money to accomplish things.”

“The past two years have brought about all kinds of unusual things happening in our businesses. We didn’t know what was going to happen with the pandemic. We didn’t know what was going to happen with the economy. And, anyone who thought they did has had a whole number of surprises since. But, here we are in 2022 and Berkshire had $7 billion of operating earnings. We’ve got 360,000 people out there who take your savings and go to work every day. They have jobs. We deliver products and you put up the money for it and deserve the rewards. You took the risks and we feel good about how things have turned out.”

Aversion to a “permanent capital loss.” “We have an extreme aversion to incurring any “permanent loss,” with your funds. The idea of losing, permanently, other people’s money. People who trust us. It’s a future I don’t want to have. We would feel terrible. We would die psychologically.”

“I can’t predict what our earnings will be and I can’t predict what the stock will do. We don’t know what the economy will do and all that sort of thing, but we do know, we want to wake up every morning and we want to be safer in terms of your eventual investment. Whether we make the most money or anything, we do not want you to get a terrible result because you’ve chosen to become our partner.”

7:15 am (Pacific) Reviewing Q1 Activities

Shareholder letter… When writing the letter to shareholders, Buffett writes the letter in his head all year long. He thinks about things he would like to tell his “partners.” Buffett has written the letter like he was sharing information with his sister Doris (now deceased). “I want to tell her what I think about the business and what I think she ought to think about it. The letter is dated February 26th and I said “not much is going on…” “

“I sent the letter out on February 26th, but I didn’t write it on February 26th and I basically wrote, ‘Not much is happening around here. We purchased some shares, but we just aren’t seeing anything.’ And, between January 1st and February 18th, as you can see, we spent $2.2 billion – half the quarter – 30 trading days. Basically, we didn’t do anything. Then, in the next three weeks, we spent $40 billion (one guy in the office does all the trades).”

“In the first part of the quarter, we spent money about $3.1 billion for re-purchasing shares. WE talked about it in the annual report. And, as Charlie would say, ‘It’s keeping us out of bars.’ It gave us something to do. We never do anything that we don’t think adds to the value to Berkshire Hathaway. So, we only re-purchase shares when that is the most attractive thing to do. We haven’t re-purchased any shares at all in April.”

NOTE: In February, not much had happened as far as changes to the business… then they purchased Alleghany…($Y)Occidental Petroleum… ($OXY) and Chevron ($CVX). They operate on a day to day business and sometimes changes can come quickly.

“Now we’re back in our more lethargic mood…”

“Anything can change at Berkshire, but the one thing that won’t change is that we will always have a lot of cash on hand. And, when I say ‘cash,’ I don’t mean ‘commercial paper.’

When 2008 and 2009 financial panic came along, we didn’t own anybody’s commercial paper. We didn’t have money market funds. We had treasury bills.”

“We believe in having cash. There have been a few times in history when if you don’t have it, you don’t get to play the next day. It’s like Oxygen. It’s there all the time, but if it disappears for a few minutes it’s all over. Our cash was down on March 31st because we spent that large sum in that brief period during the quarter – $40 billion. We committed to buy Allegheny Corp for something over $11 billion… But, we will always have a lot of cash.”

“Better than the Banks” – “Some of our companies have bank lines. I don’t know why they have bank lines? We’re better than the banks and we’ll give them the money if they need it. You know, the local bankers have been calling on them. But, there’s no reason for our subsidiaries to have bank lines. Berkshire is stronger than the banks.”

Talking about Banks/Money… “Maybe we’ll talk about this now. Money is kind of an interesting thing. People seem to like to talk to me about it. IF we put up the display. It’s a photo of a $20 dollar bill.

It says at the top “FEDERAL RESERVE NOTE.”We’ve done all kinds of things with money in this country. It’s amazing for a country only a couple hundred years old. The number of different experiments we’ve made with banks, and everything. We finally just decided to let the Federal Reserve do the issuing of money. And, down in the lower left hand corner it says, “THIS NOTE is LEGAL TENDER. FOR ALL DEBTS, PUBLIC & PRIVATE” and that makes it money. You can go in to our candy store and if you offer enough bushels of wheat we’ll probably give you a box of candy. But money is the only thing that the IRS is going to take from you. You can offer them all sorts of things and whatever, but this is what settles debts in the United States. This is the only kind of money you’re going to see in our lifetime.

Buffett displays $20 bill issued done by a bank that Berkshire ended up owning (Illinois National Bank in Rockford) signed by Eugene Abegg. But, the United States Government said this became exchangeable for lawful money in the United States. That’s what money is. It may turn out or becomes dramatically less in purchasing power. It may become almost like paper money as it has in many countries. But, when people tell you that they’re issuing new money, this is the only thing that will pays bills. Under some circumstances, and there were days in 2008, and we came very close to having a repeat of March 2020. And, we had plenty of money, but we were not very far away of having something that could have been a repeat of 2008 or something even worse.”

“We have a book store here – The Book Worm – it’s in the other room. And, they have a book called Trillion Dollar Triage. For those of you who like to read about this sort of thing, it’s a marvelous account of what took place day by day at the Federal Reserve and the Treasury. Believe me, if the Federal Reserve hadn’t done what they did – at least in my view, in a short period of time, things could have stopped.”

I tipped my hat a couple years to Jay Powell for acting as he did. You have to act with speed. In the old days, when you had runs on banks, back in the nineteenth century, a line formed and the bank would go broke. And, the guy would pay out as slowly as possible hoping something would happen…”

In Omaha, in August of 1931, four state banks closed and the national banks didn’t. They were all broke as of that day. No bank can pay off in one day all of its liabilities. But the Federal Reserve is the only one that’s good at that time. I will tell you this… Berkshire Hathaway will be there at that time. We run it on the basis that things might behave slightly less favourable. ”

The Value of the Federal Reserve... IF “Hank Paulson, George W. Bush and Ben Bernanke and a few people hadn’t taken action when they did, we were at that point where the line was formed, except it now comes in electronic form and it’s all over very fast (i.e. when there’s a run on the bank).”

The Federal Reserve is not gone during a bank run. The Federal Reserve can do whatever is necessary.”

“One time in the 1980s, I met with Paul Volker – who was a very honest man. I asked him ‘what are the limits to what you can do?’ and he said, ‘we can do whatever we need to do.”

And it’s true, that’s what happened in 2008-9 and that’s what happened in 2020 and you hope it happens again next time. But, we want Berkshire Hathaway to be there and to be able to operate if the economy stops. And, that can always happen.

COMMENT:Cryptocurrency – Was Buffett’s discussion about the legal tender and the value of the US Treasury and Federal Reserve his way of suggesting Cryptocurrencies possess no such safeguards?

COMMENT:Cryptocurrency – Was Buffett’s discussion about the legal tender and the value of the US Treasury and Federal Reserve his way of suggesting Cryptocurrencies possess no such safeguards?

7:52 am (Pacific) Questions Begin

Question #1 – from Becky – Jack Siletsky – Question about February 26th Letter to Shareholders… Little mention of activity. What happened during quarter that changed?

Charlie: – “We found some things we prefer to owning treasury bills.”

Warren: “Things developed in such a way. Read the Occidental Annual report over the weekend and decided it was a good place to put money… Bought 14% of the company in 2 weeks…”

Crazy Trends in the marketplace…

Charlie: “We have computer algorithms competing against other computers and algorithms. We have people who know nothing about stocks being advised by Wall Street people who understand even less. Why would you want your country’s public companies being traded like its a casino?”

Honeymoon… Warren: It’s funny the way things intersect. Took a trip to Las Vegas with his bride when he was 21 to the Flamingo – owned by a number of partners including Bugsy Siegel and Sam Ziegmund – who lived 2 blocks away. In fact, he was Stan Lipsey‘s uncle (ran Buffalo News – Berkshire company).

Buffett saw a number of very well dressed people – Bugsy Siegel and others came thousands of miles to do something mathematically dumb. Impossible. I thought I’m going to get rich. IF people are going to do dumb things like this.

“Nothing stranger than the operation of markets… General Theory by John Maynard Keynes he describes markets in 1936. It still describes and explains how the whole country goes about investing, speculating and gambling.

Investing is laying out money now with the hope of getting more later – deferring consumption now so you can get back more later. That’s what happens with farms. Farmers don’t buy calls, or wishing they could buy a put. They get to work on a daily business and get to tasks – just like the people who own Auto dealerships, etc. There’s roughly $40 trillion worth of ownership interests in all American business. Systems are set up and they (Wall Street) can sell you more items.

Occasionally Berkshire gets a chance to do something. It’s not because we’re smart, but maybe because we’re sane.

Charlie: In no era like the present have we had the pure gambling mechanisms that go on daily. I don’t find it valuable for capitalism.”

Warren: This is a lot better world thanks to ingenuity…

8:20 am (Pacific) Question from Section One

Question – Section 1 – “Berkshire entire companies outside of the U.S. Do you approach them or wait for them to contact you?”

Warren: We’ve taken some trips abroad looking for opportunities. $5 Billion spent on German securities… But, when we do deals in America, we can do deals in 10 minutes. Boards can be contacted quickly. Meetings held. Bit more complicated with foreign deals.

Charlie: Spent $60 billion on buying back our own shares – pretty simple investing in our own businesses at attractive prices.

8:33 am

Treating Everyone the Same (i.e. shareholders)

Years ago, Buffett wrote in the annual report that they would treat everyone the same – like partners (from Berkshire Ownership Manual).

Organization owning $101 million of Berkshire B Shares asked for a special meeting with Buffett before the AGM to discuss policies regarding ESG. Well, I’ve written lots on this, but why would they think that they would have the privilege of meeting over above others? They didn’t get a special meeting.

Question: BNSF and GEICO losing ground to Pacific and Progressive… On operating business, What are Greg and Ajit doing to address business challenges?

Greg: We have an exceptional franchise. We compete and are well aware of how they operate and the metrics that they use. We’re asking how we can best service our customers efficiently as well as in the interests of shareholders. But, I’ll put our team up against theirs any day. We continue to see long term improvements… We continue to build the franchise.

Charlie: Would you trade our operations for theirs?

Greg: Never.

Ajit: Both GEICO and Progressive are two very successful competitors. More recently, Progressive has done much better than GEICO. There are a number of reasons for that. Progressive has utilized (undecipherable) Tele…?. Advertising?

Value in Studying State Farm

Warren: GEICO is the second largest auto insurance company now. Auto insurance has become very important since 1904 Henry Ford started making automobiles. When 1936 Leo Goodwin started he wanted to get rich, but the largest insurance company was started in Illinois by a guy who knew nothing about the business and started a mutual insurance company – State Farm. It shouldn’t have succeeded according to the models espoused by the business schools. Yet, there it is. Number One.

It’s a very competitive market. State Farm ought to be studied in business schools but it refutes much of what is being taught.

Ajit is responsible for adding more value to Berkshire than Progressive’s worth.

8:53 Question – Question on Market timing. It’s impossible to time the market, yet you’ve done an amazing job of market timing 1969, 2000, 2008?”

Warren: We don’t have the feintest idea what the market is going to do when the market opens on Monday morning. We’ve never made any decision based on what the market or the economy is going to do. We spent a $50 or $60 billion during 2008. It was a significant portion of our net worth at the time. I wrote an article for the New York Times – “Buy America. I Am.”IF we had waited six months, I would have totally missed the buying opportunity.

We’ve NOT been good at timing. We’ve been reasonably good at recognizing value and opportunities when they presented themselves. We’ve never timed anything. We’ve never figured out insights into the economy…

It’s amazing what a simple game it is, but there are people who don’t benefit by telling you how simple it is. There’s a lot of value to what you can do by yourself.

Charlie: Wealth Management is a peculiar business… Some advisors are not adding value and might as well say… “Why not just give me $50,000 of your future net worth?”

The wealth management business delivers limited skills, but creates anxiety while completing “closet indexing.”

9:08 Question: Becky – Two part question. Years ago, Buffett quoted that a nuclear attack would be the greatest threat to Berkshire. What would happen if a nuclear event occurred today?

For Greg, has Berkshire suffered cyber attacks? What safeguards have been put into place?

Warren: Since 1945, small threat has existed. It is a very dangerous world when someone

Charlie: We have no way of protecting anyone from a nuclear attack. Like the guy who said, “I know what I’m going to do if there’s a nuclear attack… I’m going to crawl under a table and kiss my ass good-bye.”

Warren: Charlie’s in charge of loss recovery.

In August of 1939, there was a letter sent to President Roosevelt, about a month before the war began in Europe from Leo Szilard. The letter talked about what was happening with Jews in Germany and there was scientists being driven out including Einstein. He wonders how to get the letter to the U.S. President. He figures if he gets Einstein to co-sign the chances of Roosevelt seeing it increase. He does. The letter saying things are happening in physics with uranium and nuclear technology and America better get to it first.

There are certain things we won’t write policies on because there are things we can’t protect you against like nuclear war.

Ajit: In addition to what Warren said. What concerns me about a nuclear situation is my inability to estimate our exposure or what the implications would be. It’s very difficult to assess. We can do it with cyber attacks, etc. We can do it with fire policies, etc…

Warren: Einstein said, “I don’t know what weapons will be used in World War 3, but in World War 4, the weapons of choice will be sticks and stones.

Greg: The risk falls across all of our subsidiaries. It’s one of our greatest risk and we’re constantly monitoring and evaluating our exposure. We receive a number of attacks everyday. Rail, Energy, etc. The good news is that our teams have done an exceptional job of protecting. We have proper security protocols in place. It never stops. Significant resources are put to defending infrastructure.

Warren: My impression is you always hear business saying “government can’t do anything right” and government saying “Private business is just out for themselves.” The partnership on this front has been working.

Greg: The collaboration amongst agencies is incredibly strong. Helping us go through to see if we have bad characters getting into the system.

9:26 Station Three – Daphne from NYC 5th meeting… “Going through inflation – north of 7%. We haven’t seen this since 1982. From 1970 – 1975, your portfolios suffered paper losses. Reflecting on that, if you had to pick one stock during a period of inflation, what stock would you choose?

Invest in Yourself

Warren: I’ll tell you something even better than that one stock. The best you can do is to be the best at something. No matter if people are paying you with dollars, they’re going to give you some of what they produce for something that you produce. Whatever abilities you possess, they cannot be inflated away from you. The best investment by far is in your self. Can’t be taxed and it can’t be inflated away.

Charlie: I have some advice for you. When you have your own retirement account and your advisors suggest you put money into Bitcoin, “Just say NO!”

Warren: No one can take away the talent that you do have… Stumble into what you really like doing and what is useful to society. Then it doesn’t matter what happens with inflation or the value of the dollar.

Maintain Berkshire Culture Into the Future

9:32 Question – Becky“My family are long term shareholders of Berkshire Hathaway. How can we assess changes in the value of future management and risk/insurance assessment?

Warren: We have a culture that has worked, continues to work and it’s unique in today’s world. The shares and the shareholders will carry a long way. Berkshire is built forever. There is no finish point. People involved are here because they enjoy the work. They like being here. Why would that change?

Charlie: I remember when we had a textile mill in New England and you were dealt a hopeless hand (i.e. Berkshire Hathaway). Recognizing reality when it’s really awful and taking reasonable steps to address the problem is very important.

Warren: We dealt with a real honest guy but we made some real dumb decisions… We had wonderful people but everyone in that business had a different reference point. Some wanted to expand the company… and the whole idea was crazy.

Charlie: We reversed course.

Warren: But why did we do it in the first place.

Charlie: Probably because we were stupid.

Warren: For years, I tried a number of things in investing. Technical analysis, shorting, etc. I had tried a number of things. Then, when I was 19 or 20, I came across a book in Lincoln, NB and in this one paragraph, I saw that I was doing was doing something all wrong (referencing Ben Graham’s Intelligent Investor).

Let’s put up illusion one: Two faces vs. a Vase. The mind flips from one side to another “ambiguous illusions.” Rabbit vs. Goose.

I came across chapter 8 where Ben talked about margin of safety. I was looking at head and shoulders formations, etc. and all of a sudden you see something important and something differently. It changed my life, my way of thinking.

That’s happened in business, where I’ve looked at a company for years and then all of a sudden something changes in the way you look at things.

“Write your obituary and reverse engineer it.”

Charlie: IF you’re lucky you get a chance to correct your big mistakes. It’s so easy to overdue a good idea. That’s what happening right now: good ideas being overdone. Robinhood.

Warren: Is it wise to criticize people at all?

Charlie: “Probably not but I keep on doing it.”

LUNCH BREAK…

Afternoon Session Begins

11:00 Question – Gentleman from San Francisco – How should CEOs decide which political issues to take a stand?

Warren: Terrific question and one. I don’t put my citizenship in a blind trust when I take control of Berkshire. But, you can make people permanently mad by speaking to a temporary issue. Then, you have to consider the impact upon shareholders, employees, etc. Why would I say something that would offend 20% of the people that might take it out on our employees or shareholders if they can’t take it out on me.

So, I’ve backed off on anything on behalf of Berkshire that might have an effect on somebody else down the line upon our stakeholders.

Charlie: Even more than you I have to be very careful about what I say… chuckles, silence.

Warren: And, the different between the two of us is that I can’t resist to saying more. Papers are often reporting that Buffett is buying such and such. Well, there’s two other people who might be buying on behalf of Berkshire and the people writing it don’t have the foggiest.

Glad you asked that question. It’s a good one and I’ve probably asked

Question: Becky – from David Kass – Proposal to Tax Unrealized Gaines The Government is proposing a minimum tax on unrealized capital gains on assets over $100 million. What are your views? And, Charlie’s?

Warren: We’ll find out in a minute. We would both be affected by that tax. I have no point of view. Charlie?

Charlie: My policy is I pay whatever taxes they pass and impose upon us. I won’t be lobbying.

Warren: Lobbying is a terrible activity. I ended up lobbying once for a tobacco company (unwillingly). They didn’t care about the people of Nebraska. It was terrible. We have insurance and don’t spend Berkshire’s money on candidates you like. Don’t use it to muscle anyone else out of whatever it is you like.

Research “1989 Charlie Munger Savings and Loans letter.” We resigned from the Savings and Loans league. We said, we cannot stand what you’re doing to the country. Charlie wrote one of the greatest letters ever to come out of Berkshire.

Question: Station Five Question from Chinese national – How do you practice multi-disciplinary framework?

Charlie: It helps if you know more than one discipline. To a man with a hammer, every problem looks like a nail. You irritate people terribly when you come into their territory. Experts are resistant. I can attest to it. I’ve done it several times.

Question: Becky – From Philip Kings – Investing in an Inflationary Environment In the 1970s, you wrote an article on Fortune “How Inflation Swindles the Equity Investor.” You said stocks can’t keep pace with inflation, because all of their costs keep rising…”Comments?

Warren: Inflation swindles the equity investor, the bond investor and it swindles the person who keeps their business in cash. If you have a business that doesn’t take any capital you can charge more and keep pace, but you’re not increasing the value of the business. Our utility companies we have to take a bit more capital in order to enhance the value of the company.

I wrote that story for Fortune and it was 7,000 words and they don’t publish articles that long. I thought every word was precious and they could print it or not. They sent an editor and he said he would help edit. I didn’t move. Then, I sent it to Meg Greenfield – an old friend from the Washington Post. Meg, who is as tough as nails, said, “Warren you don’t have to tell everything you know in this article.” So, I wrote that article shorter and said more or less the same thing. IF You could have a truly stable monetary vehicle for the next 100 years, it would be better for investors and business in general.

Regarding Inflation – The best protection against inflation is still the value you cultivate in yourself.

Question – Station Six – Martin Wievent from Nashville TN. Corporate CultureCompanies get the shareholders they deserve and there is satisfaction in working for the shareholders. More ETFs and institutional investors, how do we keep the culture? Why don’t more operate like Berkshire?

Warren: Our culture is easier to keep. We have a fixed number of seats, why would we go out and recruit others to replace you? IF we had a church, and we were happy with the parishioners, we would want the same people to come back week after week. Wooing new people to come in to replace the people we already have as shareholders is crazy.

The way boards operate, it has to be process oriented. It’s extraordinary what can happen in that process, especially if shortcuts are allowed to happen (i.e. lying) things deteriorate. The Value evaporates.

Announcement: Microsoft buying Activision. When they announce it, Activision becomes a different security. It becomes a “work-out” or an arbitrage opportunity, the value or price becomes dependent upon a corporate event vs. the performance of the stock/company.

Mentions Premier W.A.C. Bennett and BC Power (BC Hydro) 50 years ago. Wondered if he was going to sell.

Buffett’s Announcement

Activision – This was an opportunity to perform a work out like the old days – they don’t present themselves very often any more. So, on January 17/18/19th whenever Microsoft made the announcement… we now own 9 1/2 of Activision. If we went over 10% we would have to complete a form file with the SEC.

This was my purchase, not a manager’s deal. We want to be clear that it was Warren Buffett’s deal. My decision… I have no idea what the SEC or the Justice Department might have to say about the deal. That’s a part of the process. But, we could lose money on the deal and it’s my call. My doing.

Question – Becky – “From Matt Figel” Growing Influence of Passive InvestingThere’s been massive growth of Passive investing through ETFs and institutional investors. Passive investing now owns over 50% of American equity. Passive managers are now the largest active owners of equities. Do you see any value to a rule that would limit their influence?

Charlie: Things are out of control and counter productive. I don’t think it’s good for the country to have 3 young Harvard graduates telling corporate executives what they ought to be doing.

Question: From Station 7 from Alburque, NM – “Want to ask about Berkshire Hathaway Energy and the unique structure. Greg’s ownership and his alignment with Berkshire. Charlie talked about aligning interests in a Harvard speech. Greg’s stake in BHE is worth more than $500 million. Is there a plan to make those shares part of Berkshire?

BHE operates with lots of leverage… If Berkshire owned 100% equity. What would change about how the company is managed?

Warren: Second part is easiest to answer then Charlie will answer first part. BHE is required by regulated utilities in different ways by different authorities to have a certain amount of debt. You can get debt money cheaper than equity money. Historically true. IF we can borrow at 3% but need to reward equity at 9%, it would result in higher prices for consumers. Regulators don’t allow and frown upon an all equity structure.

IF we owned 100% equity, we would likely expect a better rate of return.

Charlie: The other one is simple too. It’s a historical accident and it’s not a big concern. It’s not causing any breach of fiduciary. Nothing done by Greg that hasn’t also been done in the interest of Berkshire also.

Warren: We had something similar with Walter Scott at Berkshire Hathaway. Walter asked if he would want to take the public company private. We agreed on a price. His share is now owned by the estate. From our standpoint, we made a deal and have never thought that there’s been a conflict. Greg’s just not that kind of person.

Charlie: I wish we had 20 more conflicts of interest just like it.

11:55 Question Becky – Steve Blackmore Boisevin MO. How much weight do you put on China government when investing in China?

Charlie: Government of China has worried the investors from teh U.S. more in recent years than they have in previous periods. So, there’s been some tension and it’s affected some values… There are more difficulties in dealing with the regime in China than it is in China. I’ve been there because I’ve recognized the

Warren: I have nothing to add.

Question – Station Eight – Tom Ringe from Wayne PA. The Role of Float at BerkshireIn this year’s letter, you spoke about float… Question about expectations that float will be stable and cost close to zero over time. What about Berkshire’s businesses gives you confidence when competitors are trying to do the same thing?

Warren: The answer to your question is we wouldn’t be in the business unless the weighted probabilities that the float will be useful to us vs. costly to us. No one will know for a very long time. I could be wrong about it. We think the odds are pretty good and we’re quite well positioned to do so if anyone is.

Charlie: Just think about it if we could buy companies yielding 8% after tax with float money, why wouldn’t we? Relax. We’re going to have it and keep it.

Warren: Charlie recognized a time when Jack Ringwalt was upset at the regulators and wanted to sell his business. So, Charlie sent him around and I bought (National Indemnity) @ $ 50 /share.

Charlie: We really like our float.

Warren: Yes, thanks to Ajit. Who knew this guy would walk into my office in 1986 and get it to work in a way I wasn’t able to?

Charlie: The lack of bureaucracy has saved Berkshire lots of money over time and allowed us to grow.

Warren: We’ve never come close to having made a promise that we couldn’t keep. It’s a painting that I get to add to everyday. That’s a short answer to a question that I can’t remember what it was.

12:09 Question: Becky – Effects of Inflation What can American businesses do to offset the negative effects of inflation?

Warren: We’ve already talked about this a fair bit. Too much money changing too few goods. Nothing is ever exactly the same in Economics however, because people’s attitudes have been changed by the past. And, when they don’t respond the way the textbooks predict.

The federal reserve puts out a balance sheet every Thursday of all their consolidated reserves. There are currently $2.2 trillion of currency in circulation. There are 330 million people, so every man woman and child has roughly $7,000 on average. It’s a staggering sum. So, when the federal government mails out so many dollars in cash to each household in the country. After 30 days, there’s more funds circulating and they’re spending. Prices are going to go up. You don’t know they other guy got it, but you’ve got it. And, word gets around. It effects prices. It has to. It doesn’t increase the number of cars in the economy, but all of a sudden, people are out spending on items.

We are seeing an unleashing of government having mailed out a bunch of money to people. We’ve had a lot of inflation and it’s almost impossible not to have had it based on the amount of money the federal reserve has sent out to people. It’s probably better that they did it, but it’s not without consequence. Money is going to be worth less. Not worthless.

Charlie: It happened on a scale that we’ve never seen before. Those cheques were sent to anyone who claimed they had a business, but it probably had to be done…

Warren: We’re trying to build a Berksire that can withstand everything but a nuclear exchange.

12:24 Question – Station Nine – Eli Abjushakah from Montreal, QE. Accounting Protocols What would you change about GAAP rules?

Warren: I would resign the job. What is GAAP suppose to reflect and its supposed to reflect “value.” IT’s tough to do because it’s tough to be objective. It’s caused people to report what looks good in the market.

Years ago, I wrote four questions when I was on the “Audit Committee.” Four things I would want to know…

It’s not the illegal things that are outrageous, it’s the things that are “legal.” The auditors want rules and they want process so they can function. When Charlie was on the Audit committee at Solomon they had some challenges. And, their auditor was Arthur Anderson.

Charlie: They’re not around any more.

Warren: They had a $20 million shortfall.

Charlie: They called it a “plug.” When your accountant starts talking to you about a $20 million plug, you’ve got problems.

Warren: They were looking at books and had resolved Assets must equal Liabilities and it was updated everyday.

Charlie: It was a “floating plug.”

Warren: I was hoping to get a question, how could some guy be so idiotic as to buy Allegheny for $842 instead of $850? I was willing to pay $850 per share but if someone wants to charge $40 million for fees, it has to be paid by someone. There’s been two times when Berkshire’s been required to get a “Fairness” opinion. And, it was reasonable. But, one company of shareholders was different than the other. So I went to Charlie and said we need a “Fairness” opinion in this case. IF the three of us owned it we could work things out. November 27, 1978. I told shareholders that both Diversified and Berkshire shareholders would benefit from the merger. On top of that, we had to get a fairness opinion. I said to Charlie, “these things are going for $1 or $2 million,” and we need to get someone to complete it.

Charlie says, “Warren it’s very simple. Pick out ten prestigious investment banks and do exactly what I say? What do I do? Put them in order and tell the guy at the top of the list you’ll give him $60k for a fairness opinion. And, if they’re insulted by it, you’ll go down to number two and so on. And, if you exhaust the list. Start at the top and offer them $80k.”

Number one was Jack Shad. He was a very successful investment banker that I knew through Tom Murphy. So I described the procedure. And, Jack said he would do it. “We’re in.” Than EF Hutton said they would do the other side for $60K.

Charlie: They sent out an amiable alcoholic that they had to do something with.

Warren: It’s not play money and somebody has to pay, but it’s a game. And boards and corps registered in Delaware understand that it’s a way of keeping law suits at bay. So, the firms will charge whatever they can get away with.

12:50 Question Becky – Have you changed your own views on Bitcoin? My own views have evolved.

Warren: I shouldn’t answer this question but I will. I don’t want to step on your windpipe, but… IF people here owned all of the farmland in the U.S. and together they offered a 1% interest in the land for $25 billion. Or, you could own 1% of the apartment houses in the country and you offered that up for sale. You could write a cheque. Very simple. Now, if you offered me all of the Bitcoin in the world for $25, I would sell it back to you. I wouldn’t know what to do with it. It explains the difference between productive assets and speculative assets that are simply reliant upon a willingness of others to pay you for it.

Now, there are a number of frictional costs involved. And, you can do that with a lot of things. Certain things have value that don’t produce something tangible. For assets to have value, they have to produce something. In the end there’s no reason why the U.S. government – whose currency people prefer, is the only thing that’s money. Anyone who thinks that they’re going to replace the greenback as currency because they think so, they’re crazy.

Charlie: I have a slightly different way of looking at it. There are 3 things I try to avoid and those are things that are stupid, evil and make me look foolish. And, Bitcoin does all three. It’s stupid because it’s likely to go to zero. It’s evil because it undermines the Federal Reserve which we need. And, it crazy because it makes us look stupid compared to the Communist leader in China.

Warren: WE have a lot of tribal behaviour. I participate in it when I watch the local Nebraska football team. And a player might step outside the lines and the ref misses. You get tribal and it’s fun. But it get dangerous.

The last time the country was seeing this tribal was when I was a kid and Roosevelt was President. People either loved him or hated him. Roosevelt’s tribe was bigger and they did some wonderful, but I grew up in a household where you didn’t get dessert until you said something tribal about Roosevelt. And, I liked dessert.

Charlie: I live in CA and the gerrymandering is tribal. It’s made up by insane rightists and insane leftists. And, they meet every ten years and carve out ways of keeping things tribal.

Question: Section Ten – Sahedge from NJ – freshman at Rutgers…ON Finding One’s Vocation “What advice would you have for someone trying to focus on and find their calling?

Warren: That’s an interesting question because I found out early what it was what I wanted to do. I think you know it when you see it. I would tell students find out what it is you love doing and do it. Why would you spend your lifetime being around people you don’t like?

I knew I wanted to work with Ben Graham so I pestered him for about 3 years and I was prepared to work for nothing.

Charlie: Can I given the young lady some advice? Find out what it is you don’t like and try to avoid it.

Question – Becky From Tulsa OK, Oil production… We are depleting our oil reserves. Do you have concerns or comments about oil?

Warren: Charlie is the expert on oil

Charlie: IT’s hard to tell which of us is more incompetent on oil. I have a different view. I like having big reserves of oil. I would pay whatever the Arabs are charging and preserve our own. I think it’s going to be in demand over the next 200 years and we should keep it in ready supply. Nobody agrees with me, it’s just my view.

Warren: Try leaving out 11,000,000 barrels tomorrow and see what happens. This topic gets into a tribal dialogue. I think it’s nice to have some oil in this country. If you try and change over in the next 5-10 year Charlie why don’t you say something more dramatic so you’ll have offended more people.

Charlie: Some of the people supplying oil and energy in this country are some of the most reliable I wish the rest of the

Question: Station Eleven – Overflow Room. Glen Tung, shareholder from NY.Share repurchases – $1 – $3 billion per month. At a discount to intrinsic value. Any other considerations go into the share repurchases?

Warren: We haven’t bough any stock in April. IT’s something that we’ll do when we can do it and we think that we’re improving things for the remaining shareholders. Controlling factor is how much money we happen to have. We’re happier to buy shares in other businesses.

IF we had a lemonade stand and it was owned by you, Charlie and I and you said you wanted to get out, you’d name a price. If we liked the price, we’d buy you out.

Comments on Texas Pacific Land Trust – the second stock he purchased (after Cities Services Preferred).

Charlie: Warren, we’ve come a long way over a long time. And, to do that from humble beginnings with wonderful company is a favoured life.

Question – Becky Dave Shane from Brooklyn NY. Future Mergers & Deals Will Greg Able be able to act as spontaneously as you have in the future with or without board approval?

Warren: Well the board will have established the parameters they feel appropriate. (Buffett reads letter from embarrassed “independent” board member who derives salary from Directors fees while sitting on 5 boards of prestigious public companies.) Exploration of what constitutes an independent board member.

Charlie: These days, they don’t just want “independent members,” they want a duck, a cow, a rabbit. In other words, they want a diversified independent board of directors…