Happy to present an updated due diligence video on Rio-Can Real Estate Investment Trust. Rio-Can is one of Canada’s largest commercial landlords. Units of the trust can currently be purchased at a discount to NAV (net asset value). Rio-Can REIT closed today at $22.83 /unit on the Toronto Exchange (REI.UN). That ‘s about a 12% discount to book value of $25.90 as reported at the end of Q3-22.

Their future looks bright and there best days are still yet to come. It’s a good deal.

Real estate investors can go at it alone developing projects – completing zoning applications, appeasing bankers, paying for legal work, etc. Or, they can purchase units, become unitholders of Rio-Can, own a pro-rata share in some of the best placed properties in the country and ride on the coat tails of some of the country’s top real estate minds.

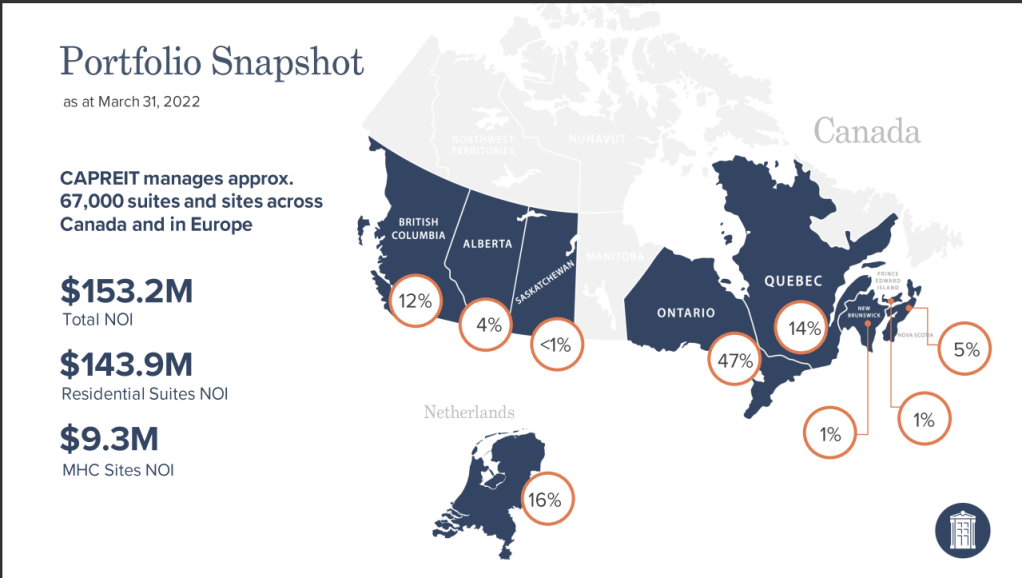

On May 17-2022, Canadian Apartment REITs published their first quarter business results. They are the last of our property portfolio “partners” to report.

In addition to being the largest residential REIT and one of the largest holdings in our real estate portfolio, CAP REIT is also the largest landlord in Canada. Their operations are a fairly telling bell weather of the residential real estate business in Canada.

As of March 31, 2022, they reported the following results:

“Following another strong and accretive year in 2021, we continued to generate solid growth and strong operating performance in the first quarter of 2022. Occupancies rose to 98.0% at March 31, 2022, up from 97.3% at the same time last year while average monthly rents increased 3.9%. Importantly, our balance sheet and financial position remained strong and resilient with a significant liquidity position.”

“Total operating revenues increased 8.4%, driven by the contribution from acquisitions completed over the last twelve months, increased stable occupancies and higher average monthly rents. Total property Net Operating Income (“NOI”) rose 4.4% compared to the same period last year. Stabilized property NOI decreased slightly in the quarter due increased weather-related maintenance costs, higher utilities costs resulting from the colder winter this year and a significant increase in the cost of natural gas, and higher property taxes. Importantly, to date we have collected over 99% of our rents, a testament to our successful initiatives to work with our residents and understand their issues through the pandemic.

During 2021, we acquired 3,744 apartment suites, townhomes and manufactured housing community sites in Canada and the Netherlands for total costs of approximately $1.05 billion. In the first three months of 2022, we further expanded our property portfolio with the purchase of 1,015 suites and sites for total costs of $439million[1]. These new properties will make a strong, accretive and growing contribution in the months and years ahead. Looking ahead, while our acquisition pipeline remains strong and robust, we will also be examining our total portfolio to determine opportunities to generate value for our Unitholders and additional capital to fund more accretive growth opportunities.”

[1] Average cost per (apartment) units purchased in Q1-2022 was approx. $432,512.31. Average cost per units purchased in 2021 was $280,448.71. That amount includes the purchase of “townhomes and MHCs,” which would explain the lower average suite cost.

This Post is published on or around May 17th, 2022, and it includes timely information that can be quickly rendered obsolete. It is FOR INFORMATION PURPOSES and simply meant to keep partners informed about some of the holdings in our portfolios. This is NOT an OFFER to purchase securities or products & NO representation is being made. Items presented may NOT be suitable for everyone. Rates change. Values will fluctuate. Please consult an experienced, qualified, licensed professional prior to investing and ensure that your investments are a part of a comprehensive plan designed to help you & your family meet your long-term financial goals & objectives.

Gordon Wiebe is registered as a “Life, Accident & Sickness” insurance underwriter with the Insurance Council of B.C, the Alberta Insurance Council & the Saskatchewan.

Of the top 0.1 percent of wage earners in America – those earning $1.48 million per year, most of them draw income from owning a regional supply business like an auto dealership or a beverage distribution company. Yes, there are celebrities, actors and athletes who make piles of money given their talent and notoriety, but three times as many affluent taxpayers make the majority of their income from business ownership. Salaries don’t make people rich nearly as often as equity does.

The nature of those businesses tends to be dull and boring including: auto repair shops, gas stations, business equipment contractors, etc. Their businesses tend to endure because they provide goods and services that meet long term needs and demands. This tends contrasts “sexy” businesses like salons, cosmetic stores, record stores, and clothing stores. These “sexy” businesses have a limited life expectancy. On average, they typically fold after 2½ – 4 years.

Another important feature of their businesses is their ability to avoid ruthless price competition – either through a monopoly or a regional advantage, etc. For instance, more than 20 percent of auto dealerships in America have an owner making more than $1.58 million per year. Those dealerships have legal protections; state franchising laws that give auto dealers exclusive rights to sell cars in a territory. Same for many beverage distributors, which act as middlemen between alcohol companies and stores and supermarkets.

The advantages of business equity isn’t lost on the owners. Most of them are happy to maintain the status quo. Turnover is minimal (i.e. don’t be looking to purchase one of these businesses at a discount anytime soon).

The author then asks, “If pop culture is right in suggesting getting rich is a path to happiness?” I’ll examine that in a subsequent blog. For now, I’m going to see if I can find a cheap distribution business.

About the Author:

Seth Stephens-Davidowitz graduated from Harvard in 2013 with a PhD inEconomics. His work has focused on using big data sources to research behaviours and attitudes. Using “big data” sources, his essay explores who are the rich in America and what relationship wealth plays in happiness (not for the faint of heart).

The Well in Toronto is Canada’s Largest Development ever. It’s Being Managed by RioCan & Allied REITs.

If anyone needed further evidence showing how uncorrelated a company’s share price (or a REIT’s unit price) can be from its underlying value, RioCan (REI.UN) provided a good example yesterday.

Net income of $160.1 million, exceeding the comparable period last year by $53.3 million

FFO (Funds from Operations) of $0.42 /unit, up 27% year of year (YoY)

A 4.1% increase in SPNOI – Same Property Net Operating Income

1.1 million sq. ft. of new and renewed leases

Occupancy was 97% – up to pre-pandemic levels

42.6 million ft2 in the “development pipeline”

16.8 million ft2 of zoning approved

2.2 million ft2 under construction

2.5 million ft2 “shovel ready”

3.2 million ft2 actively being “redeveloped”

1.7 million ft2 expected to be delivered in the next 24 months

27.4 million of new funds expected in 2022

Weighted interest costs are at 2.98%

Book Value /unit $25.96 as of March 31, 2022.

Most landlords would be satisfied with those quarterly results. So, how did the market respond to their business operations? The unit price dropped $1.15 or 5% to $20.65 from $21.80 and then closed at $20.99. It was one of the most traded issues on the Toronto Stock Exchange.

RioCanowns and operates 204 premier retail properties in Canada. They lease over 36 million square feet of space and their enterprise value is roughly $15 billion.

At $21 /unit, an investor can purchase a pro-rata interest at a discount of 19%.

Tom Gayner once commented that the secret to investing successfully is surviving the first thirty years. He was half joking and half serious, but his reasoning was sound. He suggested, after that length of time an investor would have experienced several market trends and cycles and he ought to be able to recognize their recurrence.

Since the new year, market participants have seen the following:

a hike in interest rates

a 13.5% decline in the S&P 500

a 9.5% decline in the Dow Jones Industrial Average (DJIA)

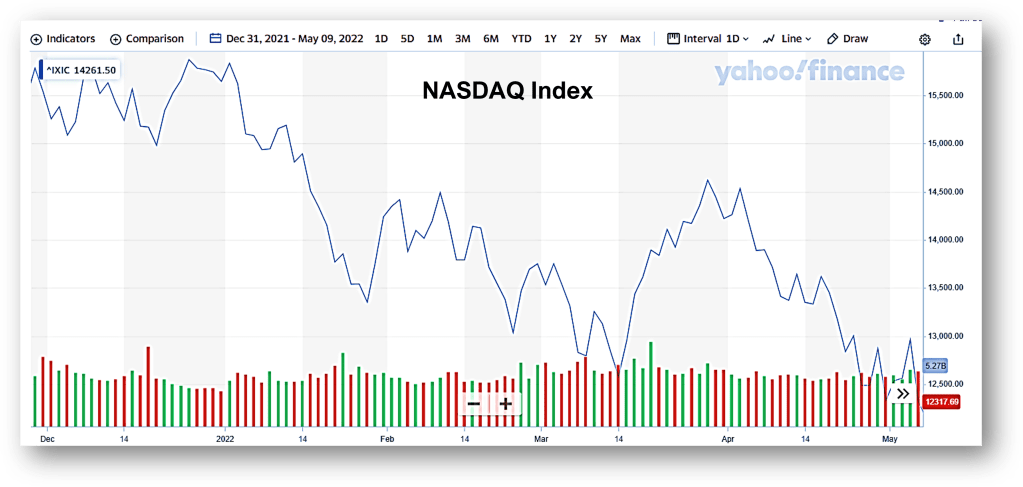

a 25% decline in the NASDAQ

None of these should come as a surprise to anyone. As Yogi Berra might say, “IT’s déjà vu all over again.”

In January 1966, the Dow Jones Industrial Average hovered around 8,891. But, by June 1982 – after years of decline, the DJIA had surrendered 72% of its value closing around 2,406. “The Nifty Fifty” – a group of cutting-edge, high-tech companies including Xerox, Polaroid, Kodak, etc. had vaulted the DJIA to lofty levels. It seems speculators were willing to pay 50-100 times earnings – not unlike some of the valuations we’ve seen in the recent market environment.

The late 1990’s also saw similar valuations placed upon countless dot.com/high tech companies as the world prepared for Y2K.

When speculation ramps up, it can drive equities to levels that simply aren’t sustainable or justifiable. Is it any wonder the NASDAQ has lost 25 percent so far this year?

Investors and speculators seeking refuge in fixed income won’t find much comfort either. If interest rates continue to rise – as they’re likely to do, bond valuations will also decline.

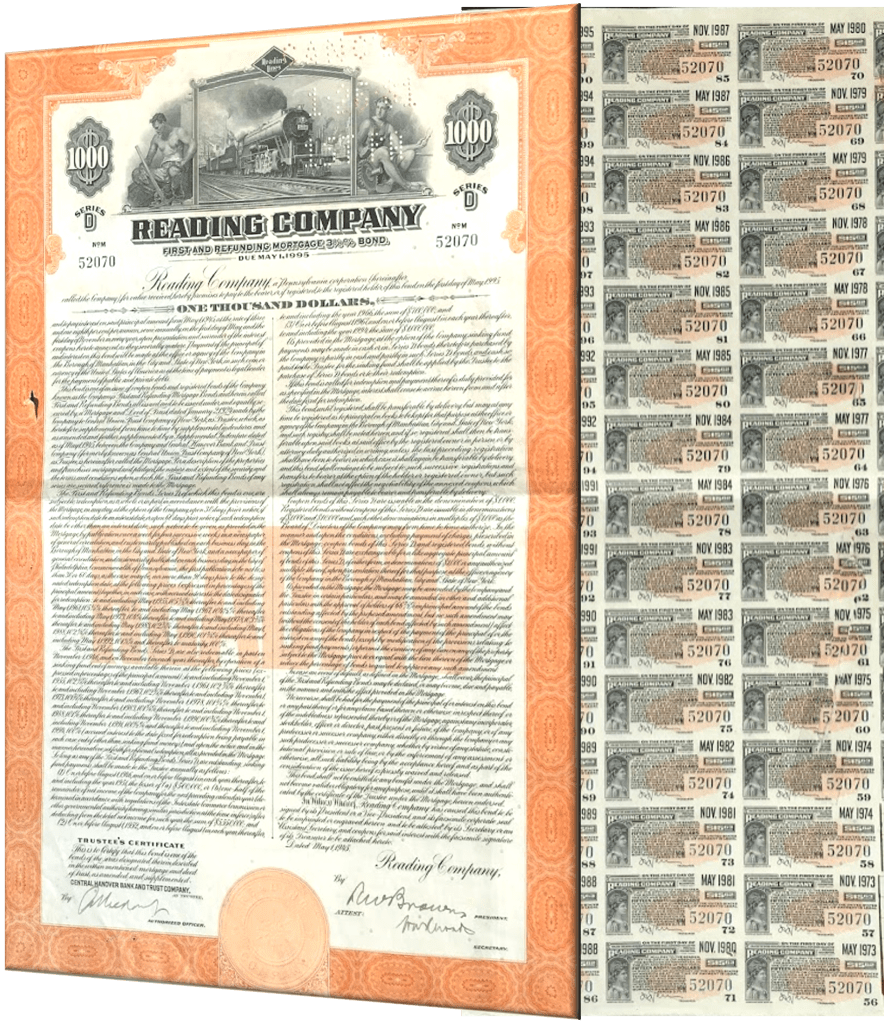

As a reminder of this, I keep a de-commissioned “50-year bond” certificate on my wall. The bond was issued in 1945 by the Reading Railroad Co. (yes, the same one from Monopoly). The bond was set to mature in 1995 and the attached coupons paid an annual rate of 3.25%.

In 1972, the bond was surrendered. The owner would have likely seen a 40% drop in the value of the bond as interest rates climbed from 5.45% in March 1972 to 6.66% in July.

It’s impossible to know what interest rates or markets will do over the short term. There are advantages to be had by studying market history and those of us over 55, have been to this rodeo before.

This morning’s Wall Street Journal ran an editorial entitled, “Warren Buffett on Wall Street Gambling. Seems the WSJ editorial board took issue with Buffett & Munger calling out Wall Street for the way they promote “gambling” activity.” They wrote:

“Warren Buffett is apparently shocked, shocked to find gambling going on in financial markets. That was the headline from the Berkshire Hathaway CEO’s remarks at its annual meeting on Saturday in Omaha. “It’s a gambling parlor,” Mr. Buffett said, and he blamed the financial industry for encouraging risky and speculative behavior.”

That Buffett and Munger called out Wall Street for croupier like behaviour shouldn’t surprise anyone. They’ve been doing it for decades. They and value investors of all stripes have long distinguished between “investing,” “speculating” and “gambling.” It’s even the first issue addressed by Ben Graham – Buffett’s teacher and mentor in The Intelligent Investor (Chapter One, paragraph 1).

For Buffett, investing means “laying out money now with the reasonable expectation that you will receive more later.” And to further quote Ben Graham, “investing is most intelligent when it is most business like.” It’s why Buffett has always made decisions based on business fundamentals, not unbridled speculation. His focus has always been on “productive assets” and he addressed that during the meeting.

Speculation on the other hand, utilizes the “greater fool theory.” You purchase some item – tulip bulbs, pet rocks, chia pets, Netscape shares, hockey cards, cryptocurrencies, NFTs, etc. with the hope that some other fool will pay you more for that item at a later date. The item’s utility is irrelevant. These ideas haven’t changed. So, what has?

Well, a few things and they tried to address some of them.

First, Charlie noted how computer algorithms compete against other computer algorithms to make split second trades. The folly of this method stems back as far as the crash of ’87, but the computers are much quicker and far more sophisticated now. The potential for loss has increased exponentially. So has the number of people effected.

Second, neither has been impressed with Robinhood or any of the quick trade, no fee apps that surfaced during the pandemic. Platforms encouraging people to make rapid fire trades without any consideration to business fundamentals is tantamount to gambling. It’s how you turn a coveted American capitalist institution like the NYSE into a gambling parlour. It’s nothing really to aspire to. As Charlie said, “We have people who know nothing about stocks being advised by Wall Street people who understand even less. Why would you want your country’s public companies being traded like it’s a casino?”

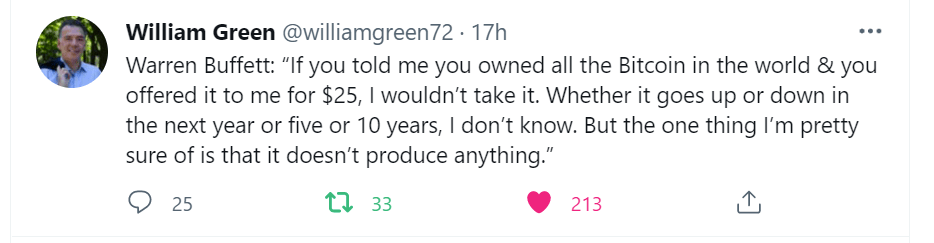

Finally, the two took aim at Bitcoin and other the cryptocurrencies. Buffett went on to explain the value of the greenback and currency that was authorized by the U.S. Federal Reserve. “Right on the bill in the lower corner it reads, “this note is legal tender for all debts, public and private.” It’s how you pay the IRS. IF you offered me all the Bitcoin in the world for $25, I wouldn’t pay it.”

The WSJ board suggested Warren and Charlie were unfairly scapegoating Wall Street and addressing symptoms vs. the actual problem. According to the board, “greed” is the real driving force and it’s not going away anytime soon as if to suggest, they’re just filling a need.

Well, that could be, but it’s not like that attitude is going to move humanity further along. I’m inclined to agree with Ben, Warren, and Charlie. Investing is most intelligent when it is most businesslike.”

Last August, J.P. MorganAsset Management released “Retirement By the Numbers,” a report that examined how investors approaching retirement manage their portfolios, their income and their spending.

The report drew on a data base of 23 million 401(k) & IRA accounts. They reviewed the activities of some 31,000 people as they approached or began retirement between 2013-2018. (401(k) and IRA are retirement accounts similar to RRSP & RRIFs).

Findings

Research from the report suggested:

a) “De-risking” is common place. Three quarters of retirees reduced their equity exposure after “rolling over their assets from a 401(k) (RRSP) to an IRA (RRIF).

b) Retirees relied on the mandatory minimum withdrawal amounts when determining how much income to draw.

c) Income and spending are highly corelated. Where income amounts were increased (i.e. from social security, pension plans, etc.) spending followed.

Retiree Profiles

The retirees studied in the report shared the following characteristics:

a) Roughly 30% of the subjects received pension or annuity income.

b) The median value of retirement accounts was $110,000.00

c) The median investable assets were estimated to be between $300,000 and $350,000.00 (i.e. balance being held in non-registered accounts).

d) The most common retirement age was between 65-70.

e) Age 66 was the most common age to start receiving Social Security.

Other Observations

The study also recognized the following trends.

First, retirees who waited until the rollover date to “de-risk” (i.e. rebalance their portfolios) needlessly exposed themselves to market volatility and the potential for loss. For example, those re-balancing their portfolios in April 2020 after the COVID pandemic, were still down 5-6% after the markets had recovered a year later. Retirees ought to consider rebalancing portfolios prior their obligatory rollover (age 71).

Second, the majority of retirees were using the RMD-required minimum distribution as a guide for withdrawal amounts versus basing amounts on retirement income needs. Like U.S. IRAs, Canada’s RRIFs are also subject to a minimum withdrawal schedule that increases with age. Retirees relying on the schedule for guidance could limit or see future income amounts reduced.

Finally, 62 year-olds represent the peak year of 9.6 million baby boomers in Canada (and the greatest years of nest egg risk are between the ages of 58-66) Should they retire and de-risk en masse, Canadian equity markets will likely undergo increased downward pressure and volatility. Retirees should consider re-balancing or “annuitizing” while markets are fully valued and prior to an increase in capital gains or interest rates.

NOTE: This blog first appeared in the October 2021 edition of the Capital Partner